About the Company

Belrise Industries Limited (formerly known as Badve Engineering Limited) is a leading automotive component manufacturer catering to two-wheelers, passenger vehicles, commercial vehicles, and electric vehicle OEMs. Established in 1996 and headquartered in Aurangabad, the company has grown into a multi-product, multi-location player with 17 manufacturing facilities across nine states.

Belrise offers a diverse product portfolio comprising:

- Metal chassis systems & Casting parts

- Polymer components

- Suspension & Mirror systems

It has long-standing relationships with domestic and international OEMs including Bajaj Auto, Royal Enfield, Jaguar Land Rover, Hero MotoCorp, VE Commercial Vehicles, Honda, Tata motors and Mahindra, holding a 24% market share in India’s two-wheeler metal components segment as of FY24. The company is also expanding into high-value EV components such as battery cases, motor housing, BMS enclosures, and charging connectors, which positions it well for the industry shift toward electrification.

IPO Details

Particulars | Details |

IPO Date | May 21, 2025 - May 23, 2025 |

Issue Type | Book Building |

Tentative Listing Date | 28-May-2025 |

Face Value | ₹5 per share |

Price Band | ₹85 - ₹90 per share |

Lot Size | 166 shares |

Minimum Retail Investment | ₹14,940 (at upper price band) |

Issue Size | ₹2,150 crore (Fresh Issue: ₹2,150 crore) |

Post-Issue Market Cap | ₹8,009 crore (at upper price band) |

Objects of the Offer

Net proceeds of ₹2,150 crore will be utilized for:

Particulars | Amount (₹ crore) |

Repayment/prepayment of certain borrowings | 1,618.18 |

General corporate purposes | 531.82 |

Total | 2,150 |

Key Strengths and Opportunities

- Strategic Expansion through H-One Acquisition: In April 2025, Belrise acquired H-One India, enhancing its design and manufacturing capabilities with high-tensile steel and body-in-white parts expertise. This adds two North Indian facilities, boosting production capacity. It expands Belrise’s OEM client base with prominent Japanese manufacturers. The move strengthens Belrise’s position in India’s growing automotive market.

- Strong OEM Relationships and EV Readiness: Long-term contracts with major OEMs like Bajaj Auto, Royal Enfield, Jaguar Land Rover, Hero MotoCorp, Honda, Tata motors and Mahindra, ensure stable demand, while an EV-agnostic portfolio positions Belrise to capitalize on the growing electric vehicle market.

- Market Leadership: With a 24% share in two-wheeler metal components, Belrise benefits from India’s growing two-wheeler market, projected to reach ₹1,767 billion globally by 2029.

- Experienced Leadership and Innovation Focus: Led by seasoned promoters with over 28 years of industry expertise, supported by a 159-member R&D team, driving innovation in EV-specific and patented products like suspension systems.

- Advanced Technology and Process Innovation: Utilizes over 700 robots, IoT systems, and poka-yoke mechanisms for precision manufacturing, ensuring high-quality, defect-free products and rapid turnaround times tailored to OEM needs.

- Vertically Integrated Manufacturing: Operates 17 manufacturing facilities across India, capacity to produce over 1,000 products, with backward and forward integration reducing supplier dependency and enhancing quality control.

Risks

- Customer Concentration Risk: Belrise Industries’ top 10 OEM customers, including Bajaj Auto and Honda Motorcycle, contributed 50.77% of revenue in FY24 and 63.82% in the nine months ended December 31, 2024. A reduction in orders from these clients could significantly impact financial performance. Losing even one key OEM client could cause a sharp decline in revenue and margins.

- Geographic Concentration: Despite a pan-India presence, 41% of Belrise’s manufacturing facilities (7 out of 17) are located in Maharashtra, making the company vulnerable to regional economic or policy changes. Natural calamities, power outages, or local unrest in the region could significantly disrupt operations.

- Raw Material Price and Supply Risk: Raw materials account for over 83% of total expenses in FY24, with significant reliance on steel, polymers, and other auto-grade inputs, all sourced on a purchase-order basis without long-term supplier contracts. This exposes the company to short-term price volatility and supply chain disruptions arising from geopolitical or production-related issues

- High Debt Levels: As of FY24, net debt stood at ₹2,259 crore with a debt-equity ratio of 0.97. Even post-IPO repayment remaining debt could strain finances if interest rates rise. High debt levels may restrict the company’s ability to invest further or withstand external shocks.

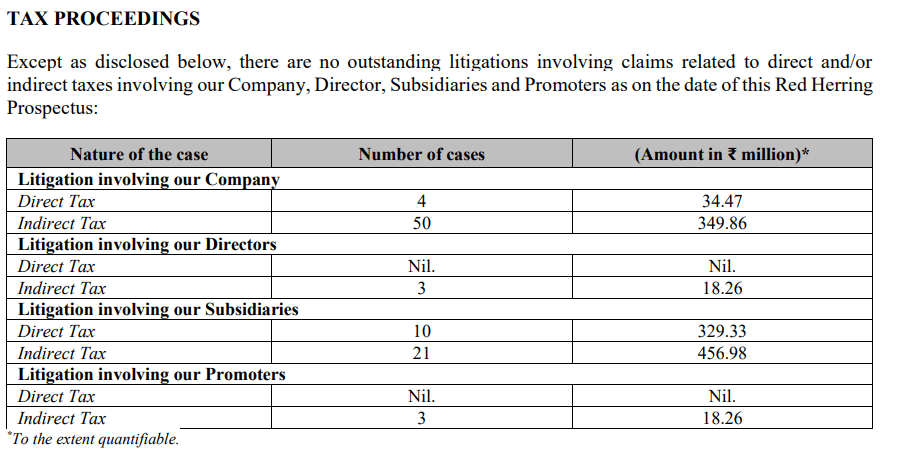

- Litigation Risks: Belrise Industries Limited, along with its directors, promoters, and subsidiaries, is involved in a number of tax-related proceedings, primarily concerning routine matters of direct and indirect taxation. While these are not considered material at present, any adverse outcome could result in financial liabilities and reputational damage, potentially affecting the company’s credibility and investor confidence.

Financial Snapshot

Particulars | 9 Month Ended | 12 Month Ended | |||

As at Dec'24 | As at Dec'23 | FY'2024 | FY'2023 | FY'2022 | |

Financial Performance Metrics |

|

|

|

|

|

Revenue from Operations | 6013.43 | 5957.88 | 7484.24 | 6582.50 | 5396.85 |

Revenue Growth (%) | 0.93% | - | 13.70% | 21.97% | 25.54% |

Earnings Before Interest, Tax, Depreciation & Amortization (EBITDA) | 767.04 | 760.00 | 938.36 | 897.66 | 763.48 |

EBITDA Margin (%) | 12.76% | 12.76% | 12.54% | 13.64% | 14.15% |

Profit After Tax | 245.47 | 297.50 | 310.88 | 313.66 | 261.85 |

Profit After Tax Margin (%) | 4.08% | 4.99% | 4.15% | 4.77% | 4.85% |

Return on Average Equity (RoAE) (%) | 9.97%* | 13.61%* | 14.18% | 16.60% | 16.44% |

Return on Average Capital Employed (RoACE) (%) | 11.03%* | 12.66%* | 14.83% | 14.04% | 12.86% |

Financial Position Metrics |

|

|

|

|

|

Net worth | 2,577.55 | 2,319.76 | 2,331.92 | 2,038.20 | 1,734.45 |

Net Asset Value (NAV) per Equity Share(₹) | 39.75 | 35.76 | 35.94 | 31.41 | 26.66 |

Total borrowings** | 2,599.80 | 2,403.36 | 2,440.98 | 2,271.40 | 2,597.96 |

Debt to Equity (no. of times) | 1.00 | 1.02 | 0.97 | 1.06 | 1.48 |

Revenue - Vehicle Type-wise |

|

|

|

|

|

2-Wheeler | 64.56% | 59.92% | 63.30% | 65.48% | 73.18% |

3-Wheeler | 2.92% | 2.04% | 2.17% | 2.09% | 2.65% |

4-Wheeler (Passenger) | 3.54% | 3.76% | 4.22% | 4.45% | 4.73% |

4-Wheeler (Commercial) | 5.66% | 4.72% | 5.01% | 5.71% | 4.99% |

Others (Auto) | 1.54% | 4.21% | 4.25% | 2.06% | 2.36% |

Others (Non-Auto) | 21.78% | 25.35% | 21.05% | 20.21% | 12.09% |

Revenue - India & International |

|

|

|

|

|

India | 75.06% | 73.20% | 76.81% | 77.92% | 86.22% |

International | 24.94% | 26.80% | 23.19% | 22.08% | 13.78% |

Total | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

* Not annualized

** Total borrowings do not include interest accrued but not due

Peer Comparison

Name of the Company | P/E (x) | P/B(x) | RoNW (%) | RoCE(%) |

Belrise Industries Limited | 18.83 | 2.50 | 13.33 | 14.83 |

Listed Peers |

| |||

Bharat Forge Ltd | 58.94 | 7.82 | 13.84 | 12.77 |

Uno Minda Ltd | 62.19 | 10.40 | 21.68 | 21.49 |

Motherson Sumi Wiring India Ltd | 39.42 | 14.98 | 42.45 | 53.25 |

JBM Auto Ltd | 45.52 | 6.97 | 22.21 | 15.15 |

Endurance Technologies Ltd | 44.76 | 6.12 | 16.24 | 18.37 |

Minda Corporation Ltd | 51.32 | 5.88 | 13.99 | 16.18 |

Conclusion

Despite Belrise Industries' strong market position and long-standing relationships with leading OEMs, its financial performance does not reflect clear growth momentum. Revenue growth has been modest in recent periods, while profitability has shown signs of pressure. A significant portion of revenue comes from a concentrated client base, making the company vulnerable to demand fluctuations. Additionally, high debt levels and multiple ongoing tax-related litigations raise concerns about financial stability and governance. While the company is investing in EV-readiness and expansion, these efforts are yet to translate into meaningful financial upside. Given the valuation and current business dynamics, we believe the risk-reward is not favorable at this stage.

Recommendation: Avoid the IPO.

Easy & quick

Easy & quick

Leave A Comment?