In an unexpected twist, Ola Electric's stock surged 15% even after reporting a net loss of ₹428 Crore in Q1FY26 (June 2025). While the headline numbers point to a continued struggle on the profitability front, the street appears to be looking ahead with optimism, driven by promising operational trends and management guidance.

Ola's Q1FY26 Performance: Losses Continue, But Green Shoots Emerge

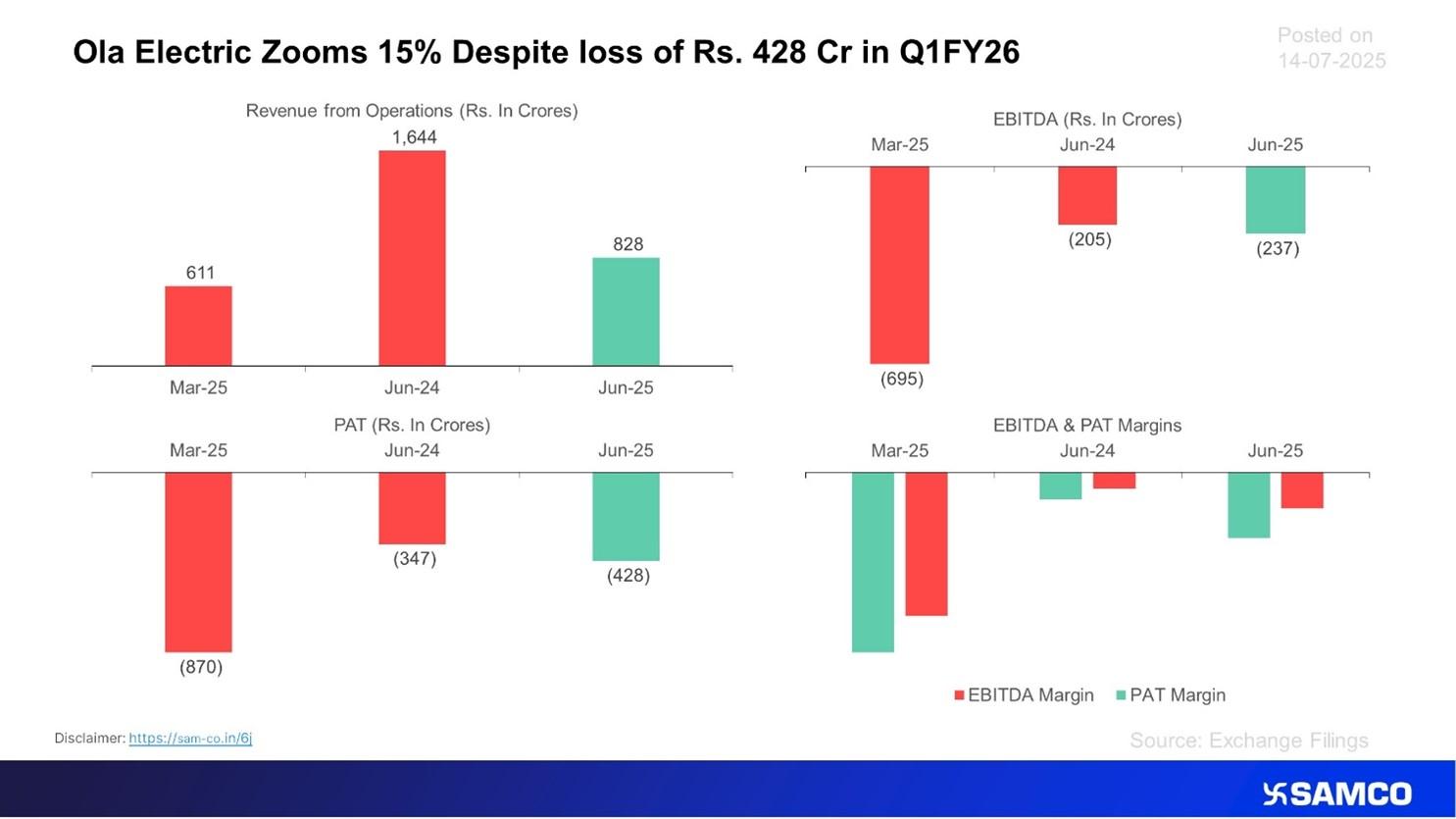

According to company filings, Ola Electric posted:

Metric | Q1FY26 (Jun-25) | QoQ Change | YoY Change |

Revenue from Operations | ₹828 crore | +35.5% | -49.6% |

EBITDA | ₹(237) crore | from ₹(695) Cr | from ₹(205) Cr |

PAT (Net Loss) | ₹(428) crore | from ₹(870) Cr | from ₹(347) Cr |

Gross Margin | 25.8% | +740 bps YoY | Improved |

EBITDA Margin | -28.6% | Better than Q4 | Weaker YoY |

PAT Margin | -51.7% | Recovery QoQ | Deterioration YoY |

Chart Insight: Despite operating in the red, Ola's margin trajectory has shown significant improvement from Q4FY25 levels, hinting at cost optimizations and better price realization.

What's Dragging Profitability?

- High Operating Expenses: Selling, General & Administrative (SG&A) expenses remain elevated at 54.5% of sales.

- Depreciation Costs: At nearly 20% of sales, depreciation continues to pressure operating leverage.

- Weak EBITDA Margins: Although sequentially better, the EBITDA margin of -28.6% still reflects poor cost absorption and inefficient scaling.

Why Did the Stock Rally 15%?

Despite disappointing earnings, the stock rallied 15% intraday. Here's why:

Management Outlook Fuels Hope

- Ola Electric aims to sell 3.25 to 3.75 lakh vehicles in FY26.

- Projected FY26 revenue stands between ₹3,400 and ₹4,700 Crore, signaling over 4x growth potential from Q1FY26 run-rate.

- High demand is anticipated for the newly launched Gen 3 scooters and the upcoming Roadster bike, especially with the festive season tailwinds.

Margin Turnaround Strategy

- Supply chain and manufacturing optimization are underway.

- Focus on cost reduction, product quality, and production efficiency.

- Management believes these changes will start reflecting in profit improvements from Q2 onwards.

Investor Takeaway: A Bet on the Future?

While the numbers don't yet paint a profitable picture, the market may be pricing in Ola's turnaround potential and first-mover advantage in India's electric mobility sector.

Bottom Line: The optimism isn't about where Ola is — it's about where it could go.

Key Takeaways for Investors

- Current Financial Health: Loss-making, negative margins.

- Sequential Improvement: Revenue and EBITDA showed positive momentum QoQ.

- Future Guidance: Aggressive FY26 targets signal confidence.

- Risks: Execution remains key — rising competition and high fixed costs could derail plans.

Outlook for FY26: Cautiously Optimistic

Ola's ability to scale production, manage costs, and maintain demand for its EV offerings will determine whether the optimism is justified. With upcoming festive demand and new product launches, the next two quarters will be crucial.

Easy & quick

Easy & quick

Leave A Comment?