Infosys has officially released the entitlement and acceptance ratios for its massive ₹18,000-crore share buyback, scheduled to remain open from November 20 to November 26. With the buyback offer price of ₹1,800 per share initially attracting strong investor interest, the final participation data paints a more realistic picture of actual gains, especially for retail shareholders.

Retail Entitlement Set at 18.1%

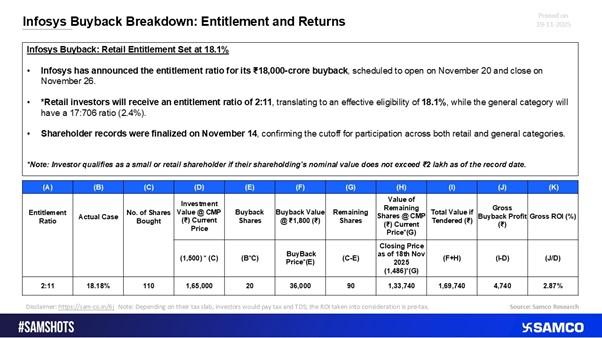

For the retail category, Infosys announced an entitlement ratio of 2:11, which translates into an effective eligibility of 18.1%.

Infosys finalized its shareholder list on November 14, marking the cutoff date for eligibility across all investor categories.

Acceptance Ratio: Only 18.18% for Retail Participants

Although the buyback price of ₹1,800 represented a significant premium over market levels, the actual acceptance ratio tells a more grounded story.

Retail investors received an acceptance ratio of just 18.18%, meaning that only around 1 in 5 shares tendered were accepted.

For example:

- Shares held: 110

- Shares accepted in buyback: 20

- Remaining shares: 90

- True gain (excluding taxes): ~2.87%

This calculation shows that even with an attractive offer price, the limited acceptance significantly reduces the overall return.

Post-Tender Price Further Reduces Gains

After the buyback window, the remaining shares in the example are valued at ₹1,486, based on the previous closing price.

This further reduces the blended gain, lowering the realised benefit for investors who expected meaningful upside.

Once you factor in:

- TDS

- Taxation on capital gains

- Opportunity cost of capital

…it becomes clear that the headline premium does not translate into substantial real-world profits for most shareholders.

Why Buyback Premiums Can Be Misleading

Infosys’s buyback highlights a crucial investing lesson:

A high buyback price does not guarantee high returns.

Key factors that truly impact investor profits include:

Acceptance Ratio

The single most significant determinant of profit in tender-route buybacks.

Post-Tender Share Price

If the stock falls after the record date, your unaccepted shares may lose value.

Real Cash Benefit

Actual return after taxes, not the advertised premium.

Market Conditions & Demand

High participation reduces the acceptance ratio, compressing returns.

In this case, although the company announced an attractive offer price of ₹1,800, the modest acceptance ratio and lower post-buyback pricing limited the effective gains for most retail investors.

Final Takeaway

While buybacks often generate excitement due to headline offer prices, the Infosys example shows why investors must evaluate entitlement, acceptance, and post-market dynamics before forming expectations.

The overall upside from this buyback remained modest, reinforcing a timeless message:

Successful buyback investing requires realistic expectations, not just reliance on premiums.

Easy & quick

Easy & quick

Leave A Comment?