India’s leading food-tech and quick commerce company posted robust results in Q1FY26, powered by rapid growth in quick commerce and strong expansion in B2C segments. The quarter marked a major milestone as quick commerce overtook food delivery in Net Order Value (NOV) for the first time in the company's history.

Adjusted Revenue Jumps 67% YoY

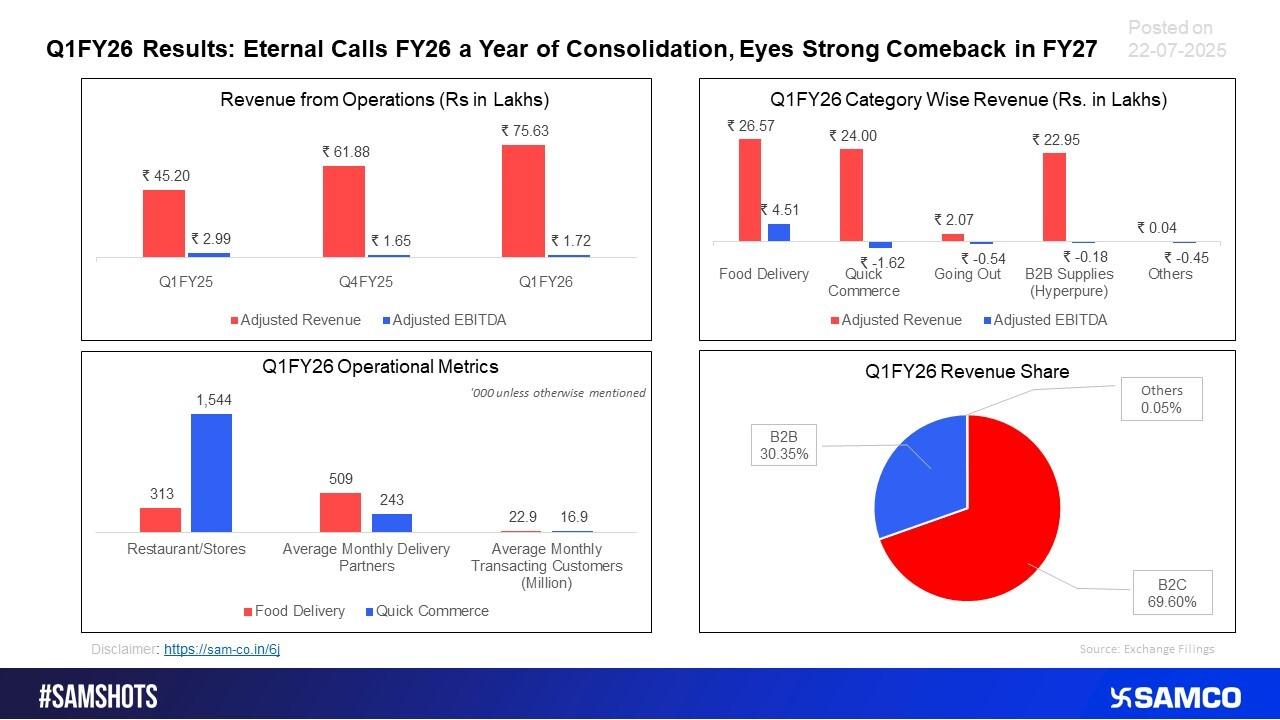

The company reported a 67% year-on-year (YoY) rise in Adjusted Revenue, reaching ₹7,563 crore for Q1FY26—up from ₹4,520 crore in Q1FY25. This also represented a 22% sequential growth over Q4FY25.

More impressively, the firm has now delivered over 50% YoY revenue growth for 11 consecutive quarters, underscoring sustained momentum across consumer-facing verticals.

Quick Commerce Emerges as Growth Engine

One of the standout achievements this quarter was the remarkable 127% YoY growth in quick commerce (Blinkit). For the first time, quick commerce NOV surpassed food delivery NOV, highlighting a clear shift in consumer preferences toward faster, smaller basket deliveries.

- Quick commerce segment loss stood at ₹42 crore, reflecting continued investment in infrastructure, dark stores, and last-mile capabilities.

- The operational metrics also tell a compelling story:

- Average Monthly Transacting Customers (MTUs): 22.9 million (Food Delivery), 16.9 million (Quick Commerce)

- Combined Monthly Delivery Partners 752,000+: 313,000+

- Restaurants

- Store Count: 1,544

- Average Monthly Transacting Customers (MTUs): 22.9 million (Food Delivery), 16.9 million (Quick Commerce)

Food Delivery Margins Improve Despite Slower Growth

While food delivery growth moderated, the segment showed healthy profitability trends:

- EBITDA margin improved to 5.0% of NOV, up from 3.9% a year ago.

- Adjusted Revenue from Food Delivery stood at ₹2,657 crore, with an Adjusted EBITDA of ₹451 crore.

- The segment continued to benefit from:

- Focus on high-margin orders

- Platform fee optimization

- Reduced discounting under the Zomato Gold program

- Focus on high-margin orders

EBITDA Under Pressure from Strategic Investments

Despite the top-line growth, Adjusted EBITDA declined 42% YoY to ₹172 crore, largely due to:

- Heavier investments in quick commerce, going-out, and new categories

- Rising marketing and operational costs

- Expansion into newer geographies and lower-penetration zones

However, the management views these investments as crucial for long-term growth and platform dominance, particularly in high-frequency categories.

NOV Crosses ₹20,000 Cr Milestone

The company’s total Net Order Value (NOV) for B2C businesses reached ₹20,183 crore in Q1FY26:

- Up 55% YoY

- Up 16% QoQ

- Quick Commerce contributed nearly half of the total NOV

With this scale, the company’s annualized NOV is nearing $10 billion, validating its leadership in India’s evolving digital commerce space.

Profit & Outlook

- The firm reported a consolidated profit of ₹25 crore, with a total comprehensive income of ₹98 crore.

- Losses in segments like Going-Out (₹48 crore) and Other Initiatives (₹45 crore) indicate the company’s readiness to absorb short-term pain for future dominance.

Looking ahead, management has revised its FY27 growth forecast, targeting 20%+ NOV growth, while aiming to try exceed 15% in FY26. The shift signals a pragmatic approach in balancing growth with sustainable profitability.

Conclusion

This quarter marks a strategic inflection point for the company. With quick commerce overtaking food delivery in NOV, and profitability improving in core operations, the business is evolving into a multi-vertical consumer platform. Despite short-term EBITDA pressures, the long-term story remains compelling—anchored in scale, speed, and customer stickiness.

Easy & quick

Easy & quick

Leave A Comment?