Q3 FY26 Performance Snapshot

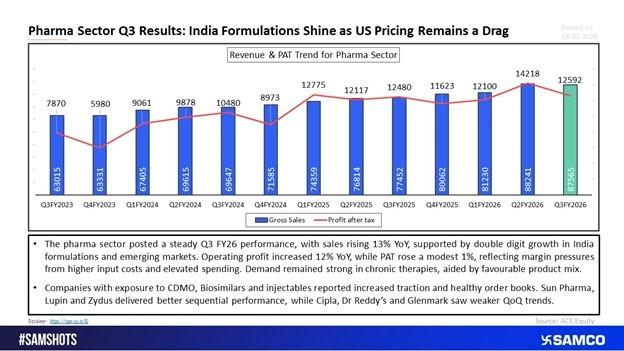

The Indian pharma sector delivered a steady Q3 FY26, with performance largely driven by domestic strength.

- Sales Growth: +13% YoY

- Operating Profit: +12% YoY

- PAT Growth: +1% YoY

While revenue and operating profit expanded in tandem, net profit growth remained muted due to margin pressures from higher input costs and elevated spending.

India & Emerging Markets Drive Growth

Double-digit growth in India formulations and emerging markets supported overall revenue momentum. Demand remained robust in chronic therapies, which continued to outperform non-chronic segments.

Key drivers included:

- Favorable product mix

- Diversification into branded portfolios

- Strong traction in domestic prescriptions

Margin Pressures Persist

Despite healthy topline expansion, profitability faced headwinds:

- Rising raw material costs

- Continued US pricing pressure in generics

- Subdued European market performance

- Higher R&D and advertising & promotion spends

Generic-focused players remained particularly vulnerable to US price erosion, limiting bottom-line expansion.

Segment Highlights

Companies with exposure to:

- CDMO (Contract Development & Manufacturing Organizations)

- Biosimilars

- Injectables

reported improved traction, healthy order books, and stronger medium-term revenue visibility.

This diversification trend is helping offset pricing challenges in traditional generics.

Company-Level Trends

- Stronger Sequential Performance:

- Weaker QoQ Trends:

Performance divergence reflects varying exposure to domestic formulations, specialty segments, and US generics.

Outlook

The sector remains structurally positive, supported by:

- Strong India growth

- Expanding CDMO and specialty pipelines

- Chronic therapy demand resilience

However, sustained US pricing pressure and rising cost structures may continue to cap margin expansion in the near term.

Overall View:

Topline momentum is intact, but earnings acceleration will depend on margin stabilization and recovery in US generics pricing.

Easy & quick

Easy & quick

Leave A Comment?