Foreign Portfolio Investors (FPIs) are key market movers in India, often signaling where smart money is headed. Their sectoral allocation can offer valuable guidance for both retail and institutional investors. The latest data from June 1–15, 2025, reveals some significant shifts in FPI behavior—some sectors are seeing substantial accumulation, while others are witnessing heavy outflows.

Let's decode the trends.

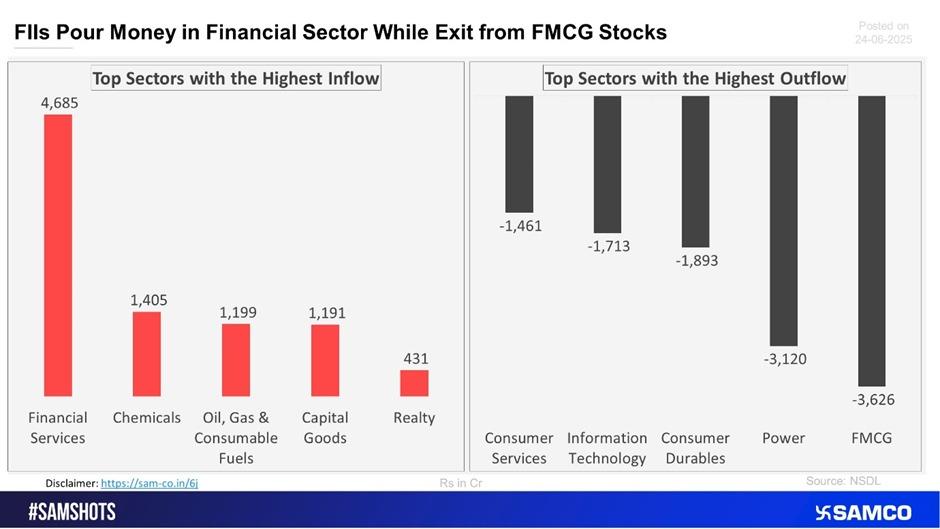

Financial Sector Leads in Inflows Despite Net Outflow

During the first fortnight of June 2025, FPIs withdrew ₹5,402 Crore overall from Indian equities. However, not every sector suffered. Financial Services witnessed the highest inflow of ₹4,685 Crore.

This strong buying could be attributed to robust quarterly earnings, attractive valuations, and India's resilient banking ecosystem. Yet, as we'll explore later, this inflow doesn't necessarily mean long-term conviction.

Other sectors that attracted capital include:

- Chemicals – ₹1,405 Crore

- Oil, Gas & Consumable Fuels – ₹1,199 Crore

- Capital Goods – ₹1,191 Crore

- Realty – ₹431 Crore

These figures suggest FPIs are still placing selective bets on cyclical and growth-oriented sectors.

Major Exit in FMCG and Power: Defensive Plays Out of Favor?

Interestingly, the same period saw massive outflows from traditionally defensive sectors.

The biggest losers were:

- FMCG – ₹3,626 Crore outflow

- Power – ₹3,120 Crore outflow

- Consumer Durables – ₹1,893 Crore outflow

- Information Technology – ₹1,713 Crore outflow

- Consumer Services – ₹1,461 Crore outflow

FMCG, which was once a stable FPI favorite, saw the largest outflow, possibly due to rising raw material costs or concerns over margin pressures. The decline in the power sector could be attributed to policy uncertainties or a cooling of demand expectations.

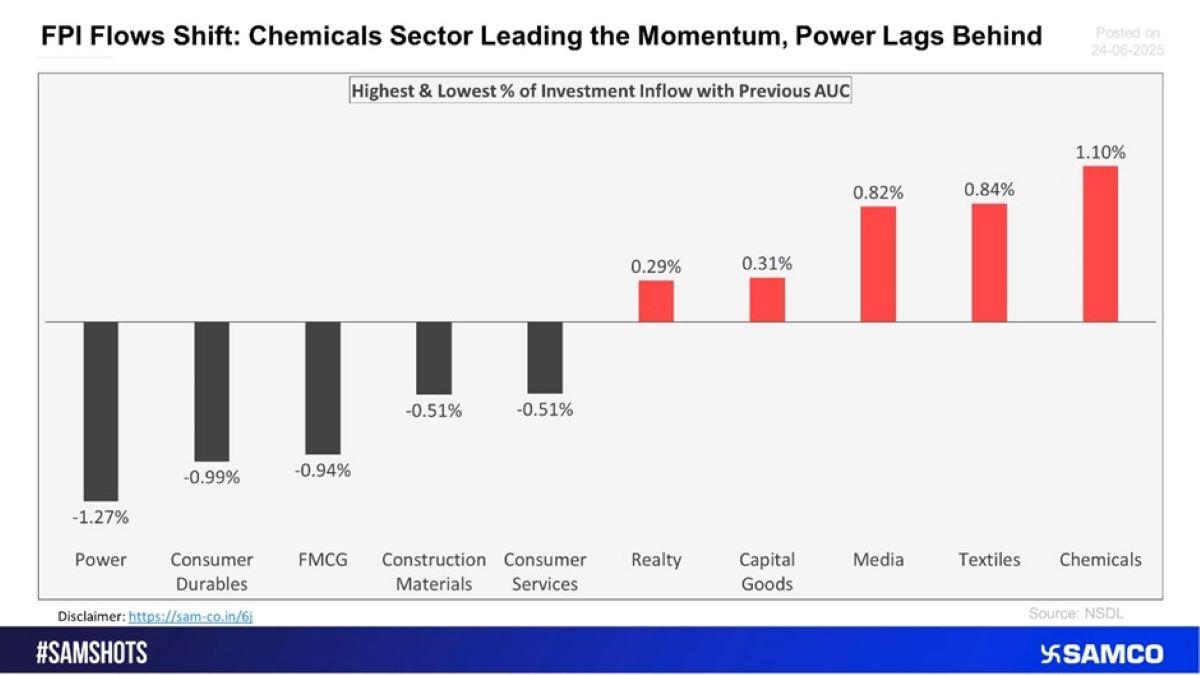

Momentum is in Chemicals, Media, and Textiles

When adjusting for Assets Under Custody (AUC), which shows the relative size of investment, the Chemicals sector shines the brightest.

Here's how the sectors ranked by % change in AUC:

- Chemicals – +1.10%

- Textiles – +0.84%

- Media – +0.82%

- Capital Goods – +0.31%

- Realty – +0.29%

These increases are especially significant as they indicate growing confidence in exports and manufacturing. For example, India's specialty chemicals sector has been increasingly gaining global attention as a China+1 alternative.

On the flip side, Power and Consumer Durables saw the most significant relative drop:

- Power – -1.27%

- Consumer Durables – -0.99%

- FMCG – -0.94%

These declines hint at lower future growth expectations in interest rate-sensitive or saturated segments.

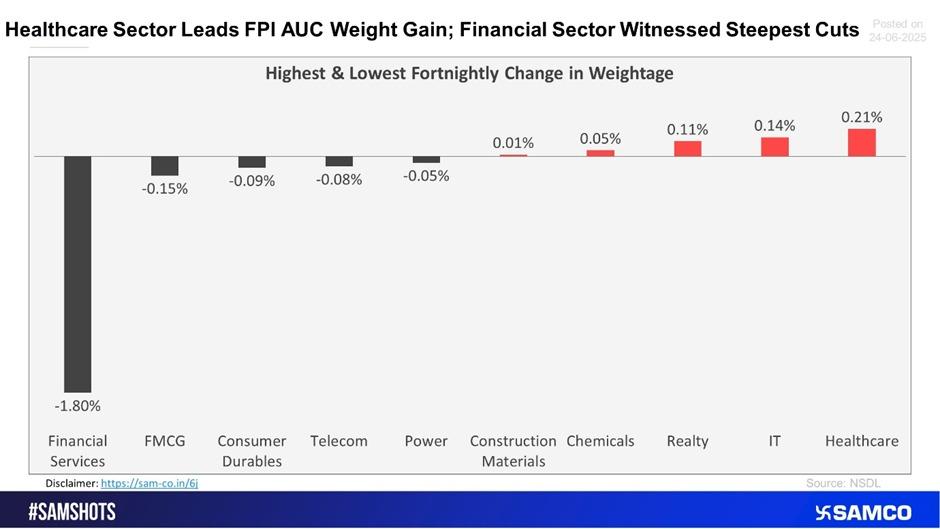

Financials See Steepest Cut in Weight – Healthcare Tops the Gains

[caption id="attachment_50011" align="alignleft" width="940"] Financials See Steepest Cut in Weight – Healthcare Tops the Gains[/caption]

Financials See Steepest Cut in Weight – Healthcare Tops the Gains[/caption]Here comes the most interesting twist.

Despite receiving the highest inflow in rupee terms, the Financial Services sector's weightage in the FPI portfolio declined by -1.80%. This suggests that while some capital flowed in, large institutional investors may have reduced their existing heavy exposure, possibly to maintain balance amid concerns about regulatory or credit risk.

Meanwhile, Healthcare led the gains in portfolio weight, increasing by +0.21%. This may indicate a defensive shift or expectation of global healthcare tailwinds.

Other notable weight gainers:

- IT – +0.14%

- Realty – +0.11%

- Chemicals – +0.05%

Sectors with minor reductions in weightage included FMCG, Consumer Durables, and Telecom.

Interpretation: What the Smart Money is Signaling

This FPI behavior tells us a few key things:

Sector Rotation Is Underway

FPIs are shifting away from traditional defensive sectors like FMCG and Power towards more growth-oriented areas, such as Chemicals, Healthcare, and Capital Goods.

Short-Term Bets vs Long-Term Conviction

Inflows don't always equal confidence—Financials received the most inflow but saw their portfolio weight drop sharply.

Export & Manufacturing Are in Focus

Chemical and Textile sectors are benefiting from global de-risking strategies and supply chain shifts.

Watch for Policy Catalysts

Sectors such as real estate and Healthcare may see further momentum if supported by government policies or budget incentives.

Final Takeaways

- FPIs pulled out ₹5,402 Crore during June 1–15, 2025, but specific sectors still attracted buying.

- Chemicals, Realty, and Healthcare saw gains in both inflow and weight.

- FMCG and Power experienced strong selling, with FMCG seeing the most significant net outflow.

- Despite inflows, the relative portfolio weight of Financial Services dropped, reflecting caution.

- Savvy investors should look beyond the headlines and focus on AUC-weighted changes for deeper insights.

Easy & quick

Easy & quick

Leave A Comment?