India’s external trade dynamics in July 2025 painted a picture of resilience on the exports front, yet stronger import demand kept pressure on the trade balance. While merchandise and services both displayed signs of stability, the widening deficit continues to underline macroeconomic vulnerabilities.

Merchandise Trade: Growth With Deficit Worries

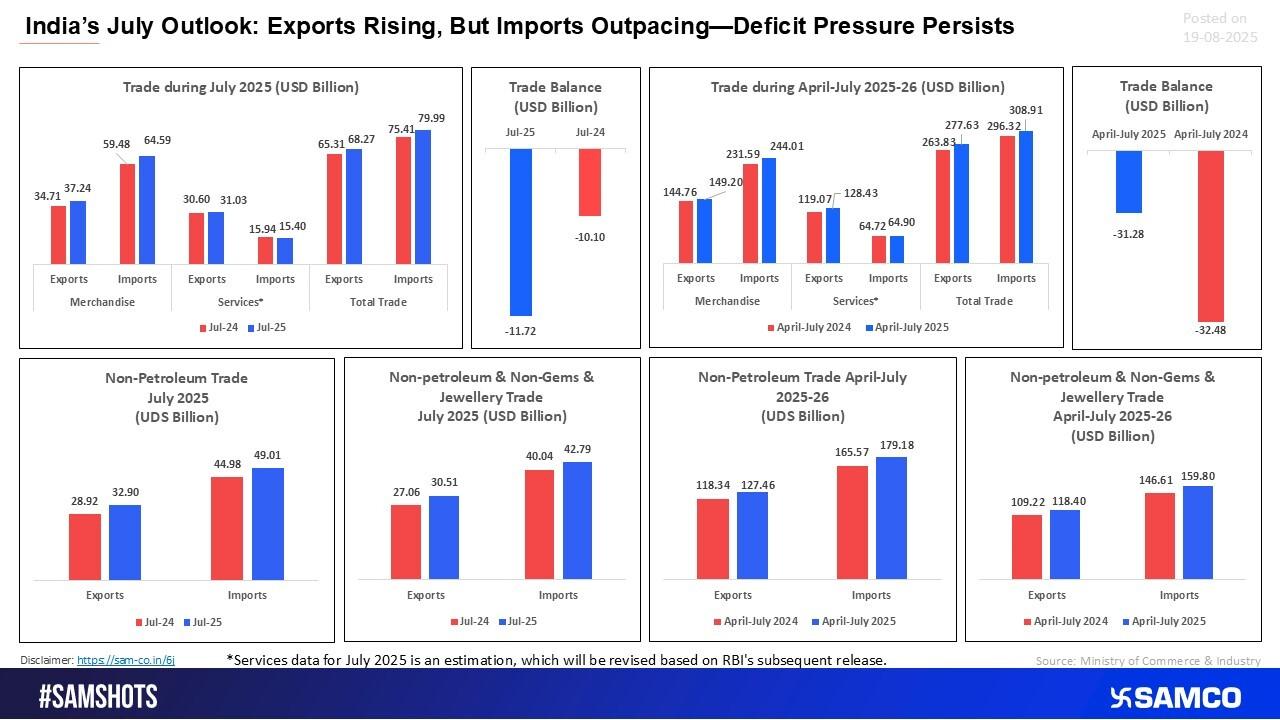

- Exports: Rose to $37.2 bn (vs. $34.7 bn in July 2024).

- Imports: Jumped to $64.6 bn (vs. $59.5 bn in July 2024).

- Trade Deficit: Widened to $11.7 bn, compared with $10.1 bn last year.

This sharp rise in imports highlights sustained domestic demand and higher global commodity costs, offsetting the export gains.

Services: Steady Cushion

- Exports: Steady at $31.0 bn

- Imports: Eased to $15.4 bn from $15.9 bn

- Net Surplus: Continued to provide a crucial buffer to merchandise deficit

The services sector remains India’s stronghold, cushioning the overall external balance.

Cumulative April–July 2025 Performance

- Exports: $277.6 bn (up from $263.8 bn in FY24)

- Imports: $308.9 bn (vs. $296.3 bn in FY24)

- Deficit: At $31.3 bn, only slightly better than last year’s $32.5 bn

Despite higher exports, imports are growing at a faster clip, keeping the gap wide.

Non-Petroleum & Non-Gems Trade: Core Strength Holding

- Non-petroleum & Non-Gems & Jewellery (NP & NGJ) exports (Apr–Jul 2025): $118.4 bn, up from $109.2 bn last year

- Non-petroleum & Non-Gems & Jewellery (NP & NGJ): $159.8 bn, up from $146.6.3 bn

Core sectors (manufacturing, engineering goods, chemicals, and textiles) continue to show resilience, proving that India’s export engine is recovering in non-commodity segments.

Investor & Market Takeaways

- Rupee Under Pressure

The persistent trade deficit is likely to weigh on the rupee, especially if oil prices remain elevated. - Export-Oriented Sectors in Focus

Sectors like IT, pharma, chemicals, and engineering goods remain relatively stronger thanks to global demand support. - Policy Watch

Continued government support via PLI schemes, trade pacts, and export incentives will be crucial to narrow the deficit. - Macro Risk Balance

Rising imports, while a sign of strong domestic demand, can complicate inflation management and monetary policy outlook.

Conclusion

India’s July 2025 trade snapshot signals a mixed trend — exports are reviving, but imports are accelerating faster, leaving the trade deficit a persistent concern. For investors, this means staying watchful on currency moves, policy responses, and export-driven sectors, as these will define the next leg of market opportunities.

Easy & quick

Easy & quick

Leave A Comment?