Key Highlights

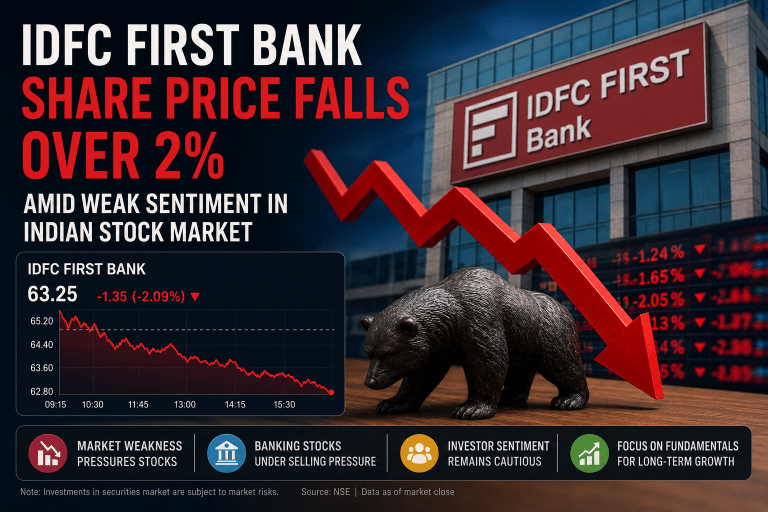

- IDFC FIRST Bank shares witnessed selling pressure amid weakness in the broader Indian equity market.

- Banking stocks remained under focus as investors assessed market sentiment, interest rate expectations, and economic indicators.

- The movement reflects broader market dynamics rather than any immediate change in the bank’s long-term business fundamentals.

- Investors should evaluate both technical and fundamental factors before making investment decisions.

Introduction

IDFC FIRST Bank shares came under pressure during trading sessions as weakness across the broader Indian stock market weighed on investor sentiment. Banking stocks often react to a combination of factors, including interest rate expectations, economic growth forecasts, liquidity conditions, institutional flows, and overall market risk appetite.

While short-term price fluctuations frequently attract attention, investors should understand the broader context behind stock movements. A decline in a banking stock does not necessarily indicate deterioration in business fundamentals. In many cases, sector-wide sentiment, profit booking, or broader market corrections can influence share prices.

This article explores the factors that may be affecting IDFC FIRST Bank shares, the bank’s business fundamentals, industry outlook, risks, opportunities, and what investors should monitor going forward.

About IDFC FIRST Bank

IDFC FIRST Bank is a private sector bank formed through the merger of IDFC Bank and Capital First.

The bank offers a wide range of financial products and services including:

- Retail banking

- Corporate banking

- Home loans

- Personal loans

- Credit cards

- Wealth management services

- Digital banking solutions

Over the past few years, the bank has focused significantly on expanding its retail banking franchise and improving asset quality.

Why Did IDFC FIRST Bank Shares Fall?

Stock prices move based on a combination of company-specific and market-wide factors.

Some reasons that may contribute to weakness in banking stocks include:

1. Broader Market Sentiment

When benchmark indices decline, investors often reduce exposure to riskier assets.

Banking stocks, due to their significant weight in market indices, frequently witness selling pressure during broader market corrections.

Factors Influencing Sentiment

- Global market weakness

- Rising geopolitical concerns

- Foreign institutional investor selling

- Weak global economic data

- Profit booking after market rallies

2. Banking Sector Rotation

Investors often rotate capital between sectors depending on market conditions.

At times, money may flow from financial stocks into sectors such as:

- Information Technology

- Pharmaceuticals

- Consumer Goods

- Infrastructure

- Energy

Such sector rotation can temporarily impact banking share prices.

3. Interest Rate Expectations

Interest rates play a major role in bank profitability.

Investors closely monitor:

- Reserve Bank of India (RBI) policy decisions

- Inflation trends

- Liquidity conditions

- Credit growth

Changes in interest rate expectations can influence valuations across the banking sector.

Understanding IDFC FIRST Bank’s Business Strategy

Over recent years, the bank has focused on transforming its business model.

Retail-Focused Growth

The bank has increased its focus on:

- Retail deposits

- Consumer lending

- Home loans

- Personal loans

- Credit cards

Retail-focused banking models often provide diversification benefits compared to dependence on large corporate lending.

Deposit Franchise Expansion

A strong deposit base is important for any bank.

Banks with growing retail deposits may benefit from:

- Lower cost of funds

- Improved profitability

- Better liquidity management

- Enhanced lending flexibility

Investors often track deposit growth as a key performance indicator.

Digital Banking Initiatives

Digital transformation remains a major focus area across the banking industry.

Financial institutions continue investing in:

- Mobile banking

- Digital onboarding

- AI-powered customer service

- Digital payments

- Financial technology partnerships

Technology adoption can improve customer acquisition and operational efficiency.

Key Factors Investors Should Monitor

Loan Growth

Loan growth indicates the bank’s ability to expand lending activities.

Strong credit demand often reflects healthy economic activity and business expansion.

Asset Quality

Asset quality remains one of the most important metrics for banking institutions.

Investors frequently monitor:

- Gross NPA ratios

- Net NPA ratios

- Provision coverage

- Loan recovery trends

Improving asset quality is generally viewed positively by market participants.

Net Interest Margin (NIM)

Net Interest Margin measures the difference between interest earned and interest paid.

A healthy NIM often contributes to:

- Better profitability

- Improved earnings growth

- Stronger financial performance

CASA Ratio

Current Account Savings Account (CASA) deposits are considered low-cost deposits.

A higher CASA ratio may support:

- Lower funding costs

- Better operating efficiency

- Improved profitability

How Market Conditions Affect Banking Stocks

Banking stocks often react more strongly to macroeconomic developments than many other sectors.

Economic Growth

Strong GDP growth can support:

- Loan demand

- Credit expansion

- Consumer spending

- Business investments

These factors may benefit banks through increased lending opportunities.

Inflation Trends

Inflation influences:

- Interest rate expectations

- Borrowing costs

- Consumer spending patterns

Investors closely monitor inflation data when evaluating financial sector prospects.

RBI Policy Decisions

The Reserve Bank of India plays a crucial role in shaping the banking environment.

Market participants monitor:

- Repo rate decisions

- Liquidity measures

- Regulatory changes

- Credit growth outlook

Opportunities for the Banking Sector

Despite short-term volatility, several structural themes continue supporting India’s banking sector.

Financial Inclusion

India continues to witness increasing banking penetration across urban and rural regions.

This creates opportunities for:

- Savings products

- Consumer loans

- Digital payments

- Wealth management services

Digital Payments Growth

The rapid adoption of UPI and digital transactions has transformed the banking ecosystem.

Banks continue benefiting from:

- Increased customer engagement

- Cross-selling opportunities

- Improved transaction volumes

Rising Credit Demand

Economic expansion can lead to increased demand for:

- Housing finance

- Vehicle loans

- SME financing

- Corporate lending

Banks positioned to capture this demand may benefit over the long term.

Risks Investors Should Consider

Every investment involves risk.

Some factors that investors should evaluate include:

Economic Slowdown

A slowdown in economic activity could impact credit growth and asset quality.

Rising Defaults

Higher defaults can increase provisioning requirements and affect profitability.

Competitive Pressure

Banks face increasing competition from:

- Private banks

- Public sector banks

- Fintech companies

- Digital lending platforms

Regulatory Changes

Changes in banking regulations can influence profitability and growth strategies.

What Does the Share Price Movement Mean for Investors?

Short-term stock movements are common in equity markets.

Investors should avoid making decisions based solely on daily price fluctuations.

Instead, they should evaluate:

- Business fundamentals

- Earnings performance

- Asset quality

- Growth strategy

- Industry outlook

- Valuation metrics

A comprehensive approach often provides better insight than focusing exclusively on short-term market volatility.

Frequently Asked Questions

Why did IDFC FIRST Bank shares fall?

The decline may be linked to broader market weakness, sector sentiment, investor positioning, and profit-booking activity rather than any single factor.

Is a fall in banking shares always negative?

Not necessarily. Banking stocks often experience volatility due to macroeconomic and market-related developments.

What factors influence banking stock performance?

Interest rates, loan growth, asset quality, deposit growth, economic conditions, and regulatory developments are among the key drivers.

What metrics should investors monitor for banks?

Investors commonly track NPA ratios, CASA ratio, loan growth, deposit growth, profitability, and Net Interest Margin.

Does a short-term decline affect long-term prospects?

Short-term price movements do not necessarily reflect long-term business fundamentals. Investors typically assess multiple factors before drawing conclusions.

Final Thoughts

IDFC FIRST Bank shares experienced weakness amid broader market pressure, highlighting how sentiment can influence stock prices in the short term. Banking stocks remain sensitive to economic conditions, interest rate expectations, liquidity trends, and investor risk appetite.

While market volatility may continue, investors should focus on business fundamentals, asset quality, growth initiatives, deposit franchise strength, and the broader outlook for the banking sector. Understanding these factors can help investors evaluate opportunities and risks more effectively while navigating changing market conditions.

Disclaimer

This article is intended solely for educational and informational purposes. It does not constitute investment advice, stock recommendations, or a solicitation to buy or sell securities. Investments in securities markets are subject to market risks. Investors should conduct their own research and consult a SEBI-registered investment adviser before making investment decisions.