Foreign Portfolio Investors (FPIs) play a critical role in shaping Indian stock market trends. Their sectoral investment patterns often serve as strong indicators of future momentum. The fortnight between 16th August to 31st August 2025 highlighted some interesting shifts — with the Auto sector leading the inflows, while Financial Services continued to face heavy outflows.

FPI Outflow at ₹14,019 Crore

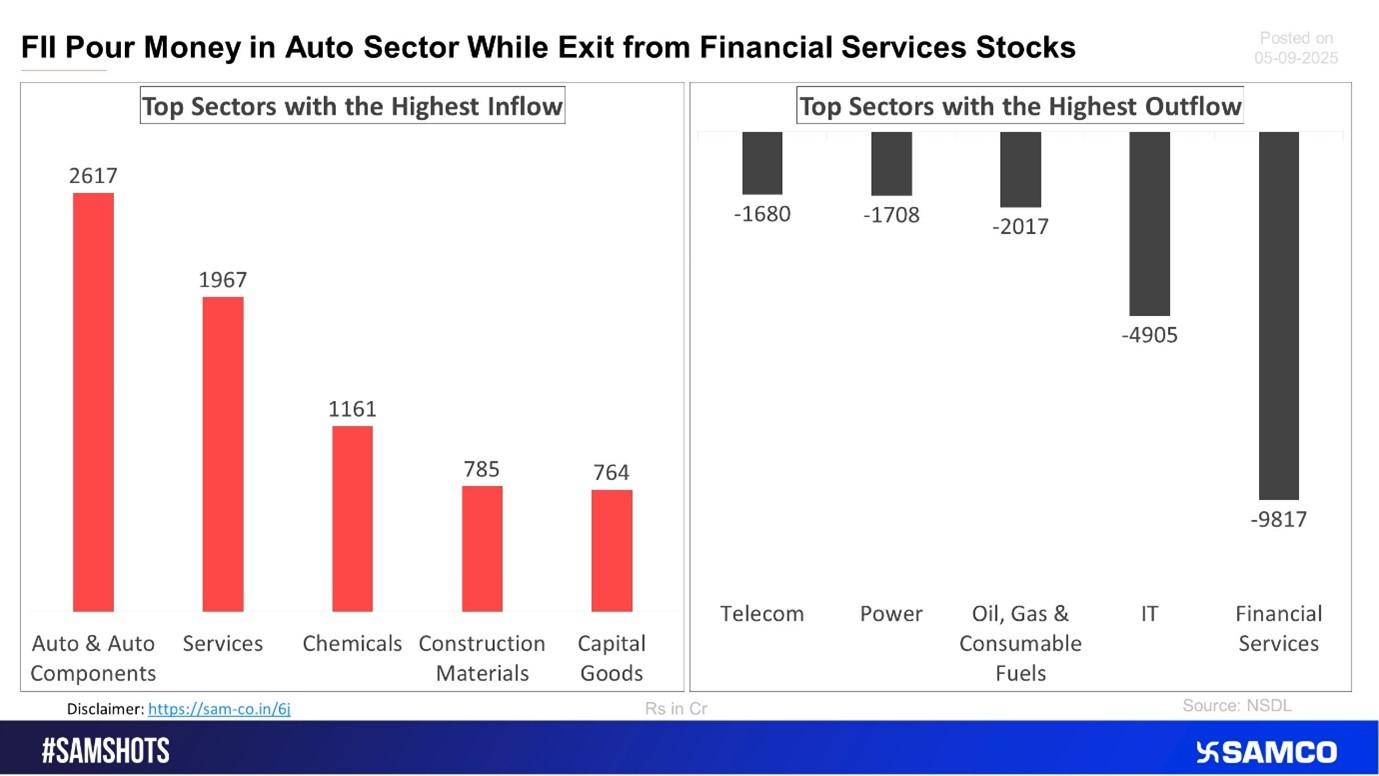

During the second half of August, FPIs recorded a net outflow of ₹14,019 crore. While this indicates a cautious stance from global investors, the distribution of flows across sectors paints a more detailed picture.

- Top Gainer: The Automobile & Auto Components sector emerged as the biggest beneficiary, attracting ₹2,617 crore of fresh inflows.

- Strong Interest: The Services sector and Chemicals also recorded healthy inflows of ₹1,967 crore and ₹1,161 crore, respectively.

- Top Loser: The Financial Services sector witnessed the largest outflow of -₹9,817 crore, marking its second consecutive fortnight of heavy selling pressure.

This clear preference for auto and industrial-linked sectors highlights investors’ tilt towards domestic growth drivers over financials.

Media Sector Shines, Textiles Lags Behind

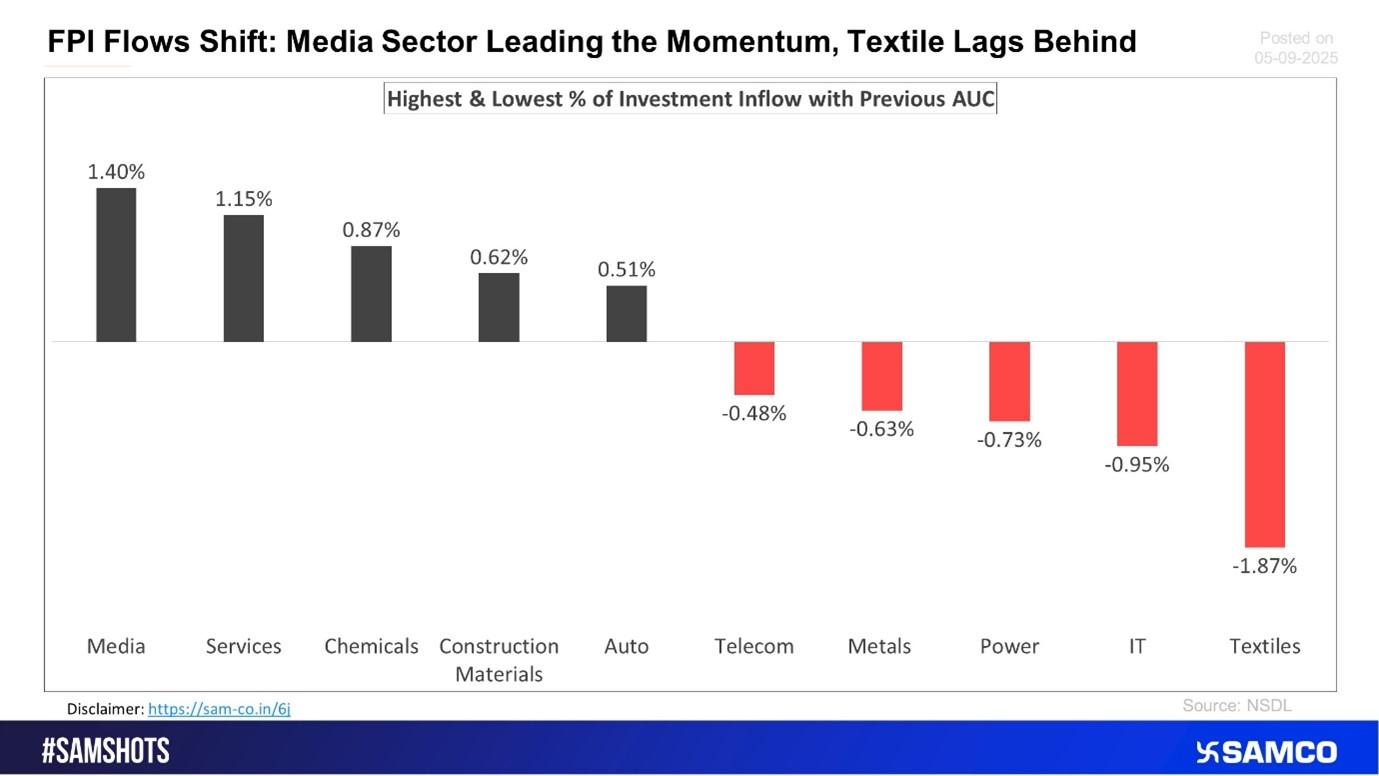

When analyzing FPI flows relative to previous Assets Under Custody (AUC), the data reveals momentum shifts:

- The media sector led the pack with a 1.40% rise in inflows compared to its previous AUC, signaling growing investor confidence.

- Services (1.15%) and Chemicals (0.87%) also attracted steady inflows.

- On the flip side, Textiles saw the steepest decline at -1.87%, followed by IT (-0.95%) and Power (-0.73%).

This shift indicates investors are betting on consumer-driven and entertainment-related growth stories, while reducing exposure to export-driven or cyclical segments like textiles and IT.

Auto Sector Sees Highest Weightage Gain

[caption id="" align="alignnone" width="1379"] Auto Sector Sees Highest Weightage Gain[/caption]

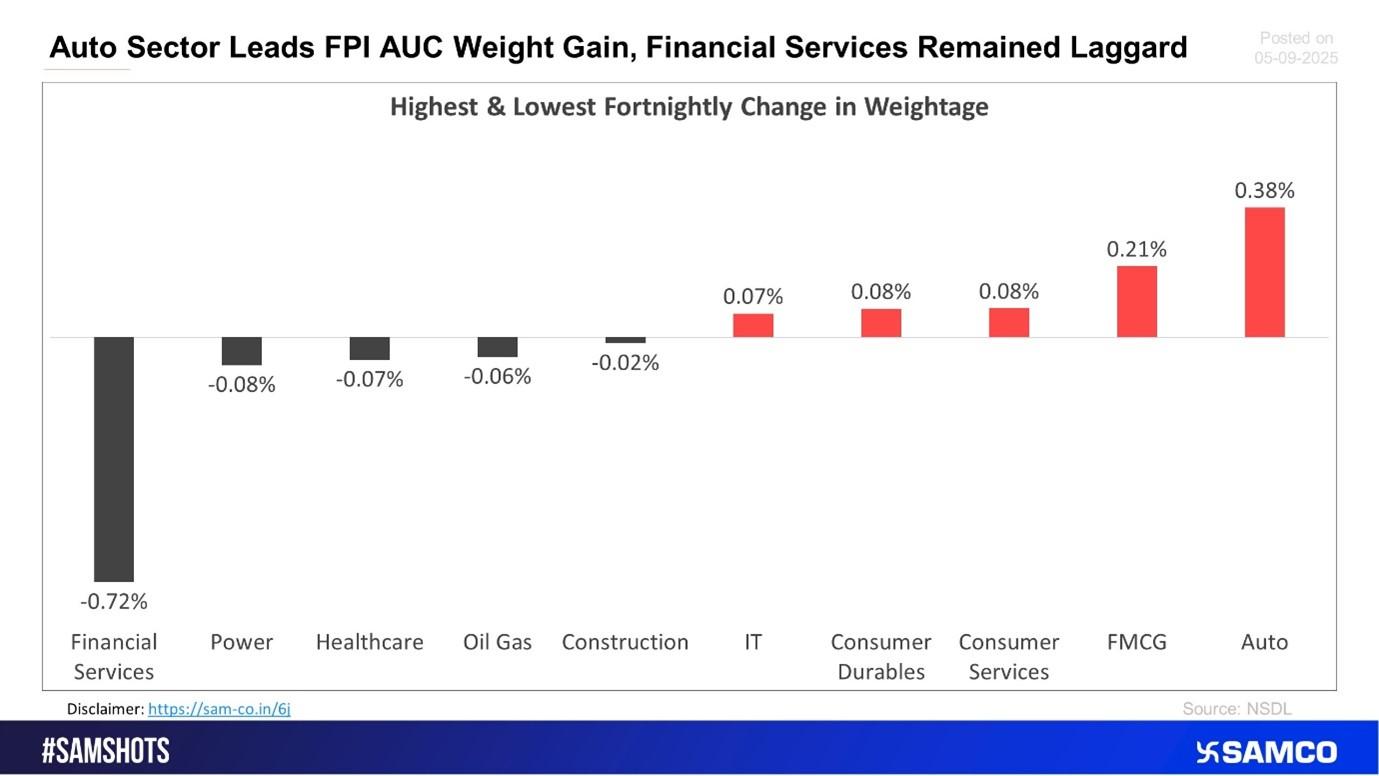

Auto Sector Sees Highest Weightage Gain[/caption]The latest fortnight also showed meaningful changes in FPI sectoral weightage:

- The auto sector recorded the highest increase in weightage at +0.38%, marking the second consecutive fortnight of strong gains.

- FMCG (+0.21%), Consumer Services (+0.08%), and Consumer Durables (+0.08%) also saw weightage gains, hinting at optimism in consumption themes.

- On the downside, Financial Services suffered the sharpest decline of -0.72%, followed by Power (-0.08%) and Healthcare (-0.07%).

The consistent rise in auto sector weightage indicates FPIs are bullish on domestic demand recovery and resilient consumer spending, while their cautious stance on financials reflects concerns over asset quality or global rate dynamics.

Key Takeaways for Investors

- Auto Sector is in the Fast Lane – Strong inflows and rising weightage highlight FPIs’ confidence in this sector.

- Financial Services Under Pressure – Consecutive heavy outflows suggest persistent caution; investors should monitor banking & NBFC trends closely.

- Media and FMCG Look Promising – Relative inflows show investors are eyeing growth in entertainment and consumption stories.

- Textiles & IT Face Headwinds – Export-driven sectors may remain volatile amid global uncertainties.

Conclusion

The fortnightly FPI data from 16th to 31st August 2025 shows a clear divergence in investor sentiment. While the Auto and Media sectors are attracting fresh money, the Financial Services and Textiles sectors are witnessing persistent selling pressure. For retail investors, tracking these sectoral flows can provide valuable insights to align portfolios with emerging market trends.

Easy & quick

Easy & quick

Leave A Comment?