In this article, we cover

- What is retirement planning?

- Why is retirement planning important?

- Why should you start planning early?

- Mistakes to avoid before you plan your retirement.

- What are the things you must look for before you plan your retirement?

- Which investment options will help you accumulate your retirement corpus?

What is Retirement Planning?

Retirement planning simply means preparing today for a golden tomorrow so that you continue to live your life the way you wish to without depending on others. So, you make a plan and invest in a systematic and disciplined manner till the age you reach your retirement. By doing so you will be able to maintain your day-to-day lifestyle without worrying about your expenses. Basically, it is said that the day you get your first pay check is the day you should start planning for your retirement. But we all have experienced this. The first pay check comes with so much optimism that saving for retirement is the farthest from your mind. As you grow older, probably in your 30s, you start to think about the time when you can sit in the balcony sipping a cup of coffee and relax for the rest of your life…that’s the time when you realise that you are already late to plan your retirement. So, before you understand what is the right age to plan your retirement, you must understand why is retirement planning even important?Why is Retirement Planning Important?

1. Stay independent during the second innings of your life

If you are born and brought up in a traditional Indian joint family, then you know that the senior citizens of the family are taken care of by the younger members of the family. But the tables have turned. Today not only is a nuclear family system preferred by young individuals but also elder members of the family plan their retirement beforehand. By doing so they can live an independent life. So, if you wish to stay independent during your retirement then you must plan for it as early as possible. Want to Retire in 2040? Invest in this portfolio of 13 stocks

Want to Retire in 2040? Invest in this portfolio of 13 stocks

2. Higher life expectancy

People these days don’t imagine entering their 90s and hence don’t count on a long retirement life. But if we look around, the average life expectancy is increasing. Many senior citizens are happily entering their 80s. Moreover, life expectancy will increase even further as we have access to the best medical facilities, better nutrition and health care. Imagine you end up working for 35 years and retire at the age of 60 with a life expectancy of 80 then you are practically spending one-fourth of your life in retirement. So, this gives you another reason to start your retirement planning early.3. Inflation is the silent killer

We all are aware of inflation by now. It silently reduces your purchasing power. So, the things you buy today for Rs. 100 will not have the same value after a few years. After 30 years from now, if the inflation rate is 7% per annum, then the value of your Rs. 100 will only be Rs. 11.34. Now, the rule of inflation applies to everything. Starting from milk to your medical bills. So, if you don’t plan your retirement smartly by considering inflation, then it will have negative impact on your finances after your retirement.Start Planning Early

Now, the question arises…when should you start planning for your retirement? The only answer you will get is - The sooner the better. Early retirement planning has its own unique benefit as you get access to compound your money. Let’s take an example. There are two individuals Mr. Raghu and Mr. Dhondu. Both of them wish to retire at the age of 60 by investing in a government pension scheme which offers a return of 8% per annum. Mr. Raghu is 40 years old and wishes to invest Rs. 4,500 per month. While Mr. Dhondu is 30 years old and wishes to invest Rs. 3,000 per month. Both of them end up investing Rs. 10,80,000 till the age of 60. Now, let’s see what will be their investment corpus?| Mr. Raghu | Mr. Dhondu | |

| Age | 40 | 30 |

| Monthly contribution | Rs. 4,500 | Rs. 3,000 |

| Rate of return | 8% | 8% |

| Total investment by the age of 60 | Rs. 10,80,000 | Rs. 10,80,000 |

| Total accumulated corpus | Rs. 26,68,263 | Rs. 45,00,886 |

Mistakes to avoid before you plan your retirement

When it comes to retirement planning, there are many mistakes or wrong assumptions people make. For instance, people in their 30s think that out of so many responsibilities there is no room for saving or investing. People in their 40s or 50s think that their children are their best retirement plan. Such assumptions lead you to nothing but an unhappy retirement. So, here are a few more mistakes or misassumptions people often carry which you must avoid before you make a retirement plan.- Not paying your debts first:If you have opted for a home loan or a personal loan or any other type of loan, the first aim you must have is to pay it off at the earliest. By doing so you will have more money to save and accordingly plan your retirement better.

- Don’t overlook health insurance: As we discussed above, with rising inflation, the cost of medical treatments will also increase. And with growing age, there are high chances that you might come across some or the other health issues. Moreover, a hefty medical bill might also dip into your savings. Hence, you must get health insurance with a decent cover.

- Limiting your retirement corpus based on a certain life expectancy: This is probably the most common mistake individuals make. While planning your retirement you must plan for a greater life expectancy so that you don’t run out of money.

What are the things you must look for before you plan your retirement?

1. How much accumulated corpus is required?

To calculate how much money you would need every year during your retirement, there is a traditional thumb rule. This rule is called the 4% thumb rule for retirement. This rule was introduced by Mr. William Bengen in 1994 in one of his research papers. Now, this rule states that accumulating money at an early age is important. But so is your spending ratio during your retirement. The 4% rule states that you must have a corpus from which you can comfortably withdraw 4% every year for your expenses. By doing so you won’t run out of money for at least 30 years. For example, if you retire by the age of 60 and you have a retirement corpus of Rs. 5 crores. You can withdraw Rs. 16 lakhs every year from your corpus so that your money can last you until you turn 90. So according to your yearly or monthly requirement, you will have to save more. But, the rule has some drawbacks. Firstly, it does not take into consideration the changing market conditions and hence there might be a situation where you might run out of money before 30 years of your retirement. Secondly, if you have an asset allocation in which you have a specific lock-in period then this rule might not work for you. So, what is the other alternative to decide how much corpus will you need post-retirement? Here are a few steps you could follow:- Make a list of expected expenses you will incur during your retirement. This will include things like groceries, utilities, medicine bills, clothing, house maintenance and a yearly vacation.

- Calculate expected income after retirement such as pension, rent and income from investments.

- Calculate net income needed in retirement. So for example, you expect an expenditure of Rs. 50,000 per month and your income is Rs. 25,000, then you will need Rs. 25,000 more.

- As we had discussed earlier, inflation is a silent killer. Today’s Rs. 25,000 will not have the same purchasing power tomorrow. So, to calculate the future value you need to take into consideration the impact of inflation. You can take an average inflation rate of 7% annually. Accordingly, you can easily calculate the amount you will need every year post retirement.

Best Retirement Plans for You

2. Identify your risk appetite

Once you know how much retirement corpus you will need, the next thing to do is to invest and accumulate this corpus. Few individuals might start planning their retirement at the age of 20 while few might start at the age of 35 or 40. So accordingly, each individual will have a different amount of disposable income for investing. Disposable income is simply the amount you are left with after spending on your needs. According to your age and the disposable income available, you must decide for yourself whether high-risk, low-risk or medium-risk investment options will suit you the best. If you are in your 20s, you may have fewer responsibilities and minimum disposable income. So, you can afford to take a little more risk and invest in equities to generate the highest returns with a higher impact of the power of compounding. If you are into your 30s, don't worry you still have 30 more years until retirement. At this age you can still invest in direct equities but remember to diversify your portfolio a little bit by allocating your corpus towards stocks of different sectors. Or you could simply invest in an equity mutual fund such as a flexi cap fund. Don’t fall prey to any random mutual fund which assures that they would create wealth for you. You must invest in the right mutual fund which has the ability to outperform and generate returns for you. To know which is the Sahi mutual fund, simply visit www.rankmf.com or click here. Apart from investing in equities, you must also diversify a part of your portfolio towards fixed income instruments like bonds. This allows you to create a hybrid portfolio with exposure to both equity and bonds. If you are in your 40s then you may be at the peak of your career with a hefty salary in hand. With a higher disposable income, you can make a better contribution towards your retirement planning. At this stage, you must partly shift your focus towards capital protection rather than wealth creation. So, you can increase the exposure to large-cap stocks rather than investing in small or mid-cap stocks. And shift a bigger part of your portfolio towards bonds. And if you are in your 50s, then retirement is just around the corner. It’s time to focus entirely on capital protection. So, you can minimise your asset allocation towards direct equity and shift your capital to invest in debt instruments or government pension schemes.Two Most Popular Government Pension Plans

1. Senior citizen saving scheme

The Senior Citizens Savings Scheme (SCSS) is a scheme launched by the government of India with the main aim of providing senior citizens with a regular income after the age of 60. Benefits of investing in SCSS| Minimum investment amount | Minimum Rs. 1,000 and in multiples of 1,000 Maximum Rs. 15,00,000 |

| Eligibility | - Individuals who have attained the age of 60 years or above. - Individuals who have attained the age of 55 years old, but are below the age of 60 years old and have retired on superannuation - Retired defense services personnel |

| Tax benefits | Up to Rs. 1,50,000 under section 80C of Income Tax Act, 1961 |

| Interest rate | 7.4% per annum |

| Tenure | Minimum 5 years Premature withdrawal is allowed |

2. Pradhan Mantri Vaya Vandana Yojana

This is another scheme which is launched by the Government of India with the main aim of providing senior citizens with a regular source of income after the age of 60. Benefits of investing in PMVVY| Minimum investment amount | Rs. 15,00,000 per senior citizen |

| Eligibility | Individuals who have attained the age of 60 years or above. |

| Tax benefits | Up to Rs. 1,50,000 under section 80C of Income Tax Act, 1961 |

| Interest rate | 8% per annum |

| Tenure | 10 years, premature withdrawal is allowed. |

| Loan | Available after completion of three policy years |

- LIC pension plan

- SBI pension plan

- HDFC pension plan

- SBI life retire smart

- SBI life saral pension plan

- LIC retirement plan

- UTI retirement benefit pension fund

- LIC monthly pension plan

- HDFC life pension guaranteed plan

- SBI retirement plan

- ICICI pension plan

- SBI life pension plan

Think Beyond Pension Plans for your Retirement

Bottom line

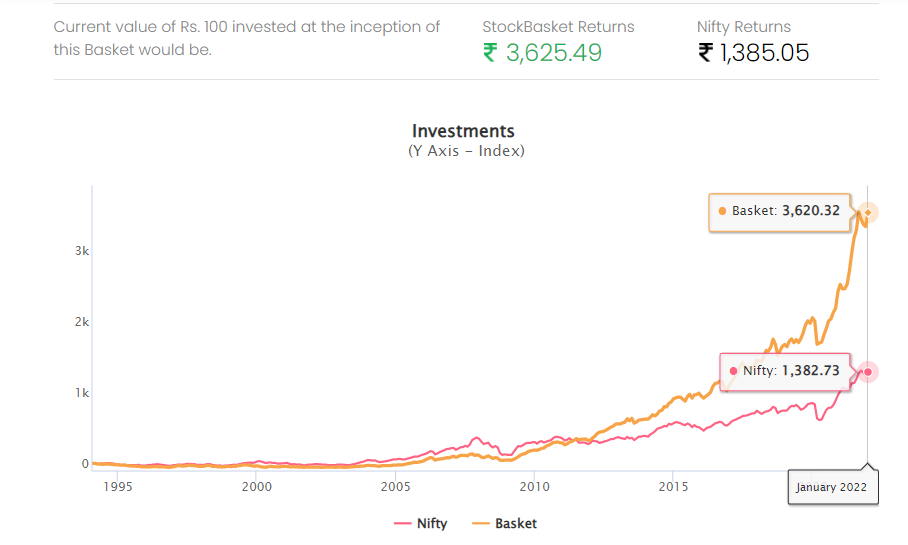

Retirement planning is indeed a crucial part of life and so is building your retirement corpus. As we just saw, no matter the age, we all have exposed a certain part of our portfolio to equities. Hence while researching the best stock you must put yourself in the role of a Sherlock Holmes and unwind a financial mystery as the right stock will only have the ability to generate wealth for you. After investing you will also have to keep monitoring your portfolio every now and then. To save you from the trouble of researching, selecting and monitoring your investments we have introduced StockBasket. StockBasket is India’s first long-term buy and hold investing platform. It has expert-curated baskets of stocks or mini portfolios of top quality companies for you to invest in just a few clicks. We also have one such retirement focused basket - Retire in 2040 basket. This basket is expertly curated with quality stocks of 13 companies.

A glimpse of the portfolio:

| Stocks | Weightage |

| Coforge Ltd. | 19.43% |

| Larsen & Toubro Infotech Ltd. | 12.10% |

| Asian Paints Ltd. | 11.93% |

As you can see the retirement basket has outperformed the Nifty50 index almost 3 times since inception. Click here to explore the basket now.

To invest in StockBasket all you need to do is Open a free demat account with Samco. It’s time for you to plan your retirement smartly!

As you can see the retirement basket has outperformed the Nifty50 index almost 3 times since inception. Click here to explore the basket now.

To invest in StockBasket all you need to do is Open a free demat account with Samco. It’s time for you to plan your retirement smartly!

Leave A Comment?