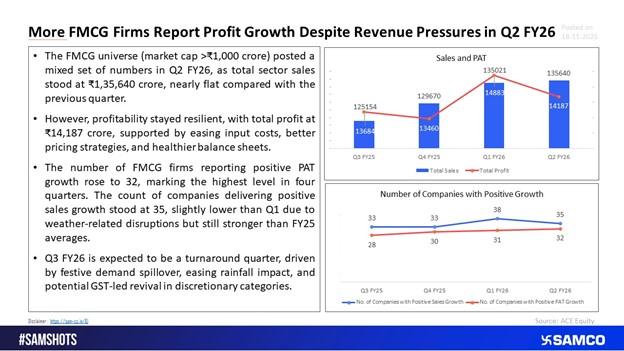

The FMCG sector delivered a mixed performance in Q2 FY26, reflecting the impact of erratic rainfall, GST rationalisation effects, and softer rural demand. While sector sales remained nearly flat at ₹1,35,640 crore, the broader profitability picture showed resilience as companies benefited from easing raw material costs and stronger balance sheets.

Weather & GST Hit FMCG Revenue Traction in Q2 FY26

The sector’s overall revenue stagnation in Q2 can be attributed to:

- Unseasonal and excessive rainfall is disrupting distribution and retail activity

- GST rationalisation influencing channel stocking patterns

As a result, quarterly sales remained broadly unchanged from the previous period, indicating stress on topline performance across major FMCG segments.

Profitability Remains Strong Despite Revenue Pressures

Even as revenue softened, total sector profit rose to ₹14,187 crore, supported by:

- Easing input costs, especially in edible oils, packaging materials, and chemicals

- Improved pricing strategies and premiumisation-led margin support

- Better cost controls and more efficient supply chain management

- Healthier balance sheets, reducing finance cost pressures

This profit resilience demonstrates that FMCG companies continue to benefit from operational efficiencies and improved input cost dynamics.

More Companies Reporting Positive PAT: Highest in Four Quarters

A key highlight of Q2 FY26 was the improvement in company-level performance indicators:

- 32 FMCG companies reported positive PAT growth, the highest in the last four quarters

- 35 companies reported positive sales growth, slightly lower than Q1

- The dip was primarily due to weather-related distribution challenges

- However, this number still remains above FY25 averages, showing improving sectoral momentum

- The dip was primarily due to weather-related distribution challenges

This indicates that while broader revenue growth was muted, the underlying performance of individual companies showed encouraging signs of recovery.

Outlook: Q3 FY26 Likely to Mark a Turnaround

Industry analysts expect Q3 FY26 to witness notable improvement across both sales and profitability due to:

- Festive demand spillover, especially in discretionary FMCG categories

- Normalisation of rainfall patterns, improving rural consumption

- Potential GST-led revival, benefitting personal care, home care, and packaged foods

- Better inventory flow and channel restocking, aiding volume growth

If these trends sustain, the FMCG sector may enter a stronger growth cycle in the second half of FY26.

Conclusion

Despite revenue pressures in Q2 FY26, the FMCG sector showcased robust profitability and improving company-level performance. With easing cost headwinds, festive momentum, and stabilising market conditions, the outlook for H2 FY26 remains optimistic. A potential demand revival—particularly in rural and discretionary categories—could set the stage for a more broad-based recovery in the coming quarters.

Easy & quick

Easy & quick

Leave A Comment?