FPI Sectoral Trends (Feb 1–15, 2026): Clear Rotation Toward Domestic Growth Themes

Foreign Portfolio Investors (FPIs) displayed a decisive sectoral rotation during the first fortnight of February 2026, signaling a strategic shift toward domestic growth, infrastructure, and cyclical sectors. With total net inflows of Rs 19,675 crore, the pattern reflects growing confidence in India’s capex cycle and domestic demand outlook, while exposure to export-oriented and defensive sectors was reduced.

This sectoral repositioning offers valuable insights for investors tracking institutional money flows and emerging market trends.

Overall FPI Flow Trend: Domestic Themes in Focus

The latest data indicates a clear preference for sectors linked to:

- Infrastructure and capital expenditure

- Domestic economic growth

- Investment cycle revival

- Financial intermediation

At the same time, sectors dependent on global demand or considered defensive saw profit booking and allocation cuts.

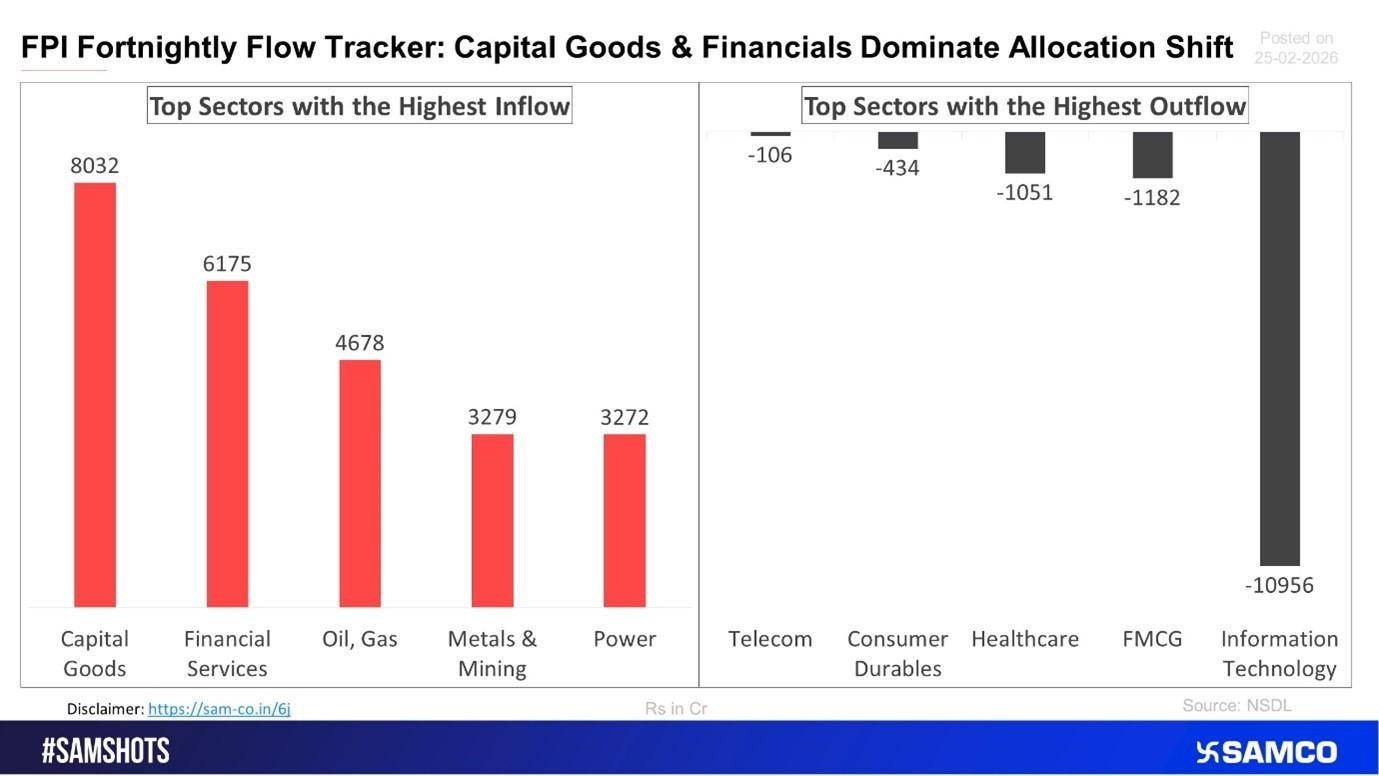

Top Sectors That Attracted FPI Inflows

1. Capital Goods – The Clear Leader

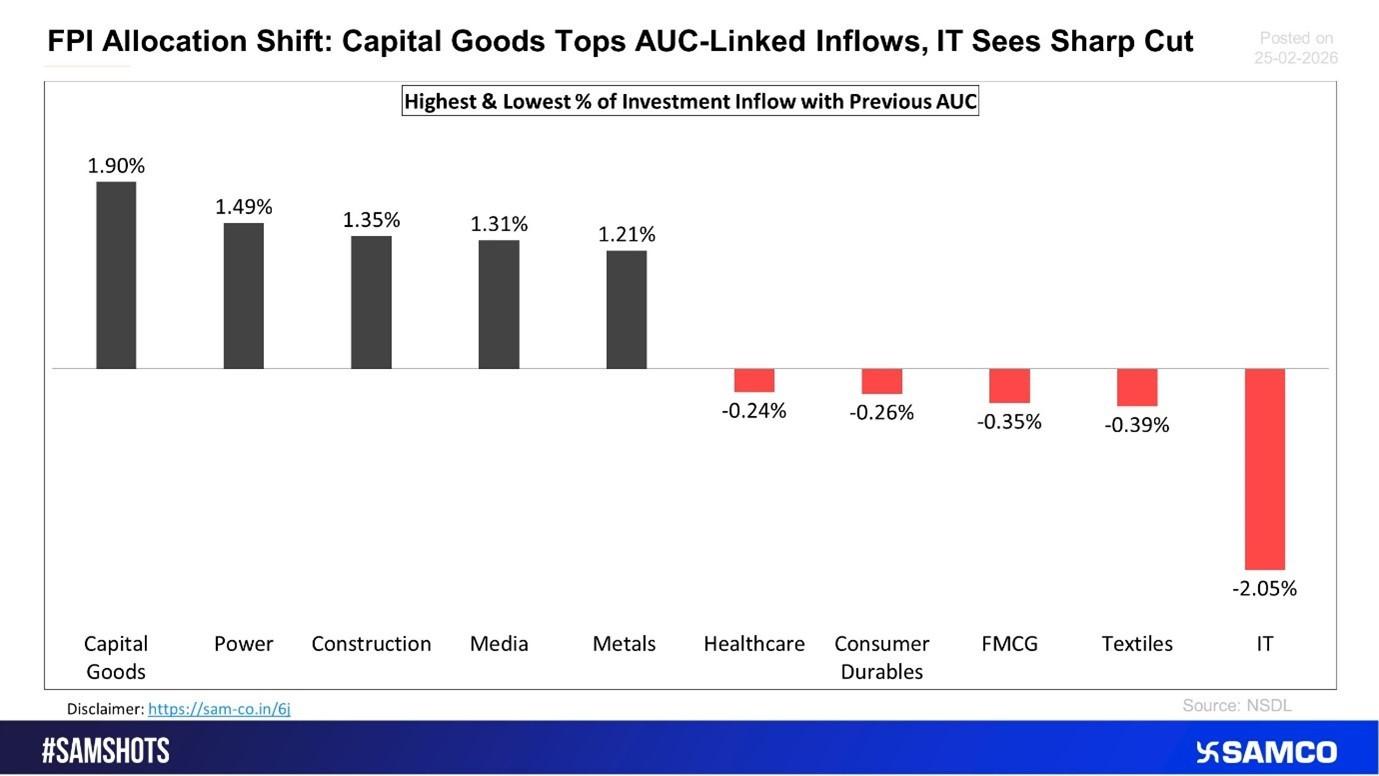

Capital Goods emerged as the top beneficiary, with net inflows of Rs 8,032 crore. On a relative basis, the sector recorded the highest incremental allocation at 1.90% of prior AUC, highlighting strong institutional conviction in India’s ongoing capex cycle.

The inflows reflect optimism around:

- Government infrastructure spending

- Private sector capacity expansion

- Order book visibility for engineering and industrial companies

2. Financial Services – Strong Institutional Interest

Financial Services saw robust inflows of Rs 6,175 crore, reinforcing the sector’s importance in the domestic growth story.

Key drivers include:

- Credit growth momentum

- Improving asset quality

- Strong earnings visibility

- Beneficiary status in a rising investment cycle

3. Oil & Gas – Tactical Allocation

The Oil & Gas sector attracted Rs 4,678 crore, indicating tactical positioning amid stable energy demand and improving profitability dynamics.

4. Metals, Power, and Infrastructure Plays

Other cyclical sectors that saw steady accumulation include:

- Metals & Mining: Rs 3,279 crore

- Power: Rs 3,272 crore

- Construction: 1.35% AUC-based allocation increase

- Media: 1.31% increase

Power recorded a strong relative inflow of 1.49% of prior AUC, reflecting expectations of sustained electricity demand and capacity expansion.

Sectors Facing FPI Outflows

1. Information Technology – Major Profit Booking

The IT sector witnessed the sharpest selling pressure with Rs 10,956 crore in net outflows. Relative allocation declined by -2.05%, while portfolio weight fell by -1.29%.

The trend suggests:

- Profit booking after previous rallies

- Cautious outlook on global demand

- Rotation toward domestic themes

2. FMCG and Other Defensive Segments

Defensive sectors also saw moderate selling:

- FMCG: Rs 1,182 crore outflow (-0.35% relative allocation)

- Healthcare: Rs 1,051 crore outflow (-0.24%)

- Textiles: -0.39%

- Consumer Durables: -0.26%

- Telecom: Marginal outflows

The shift indicates reduced preference for safety plays in favor of growth-oriented sectors.

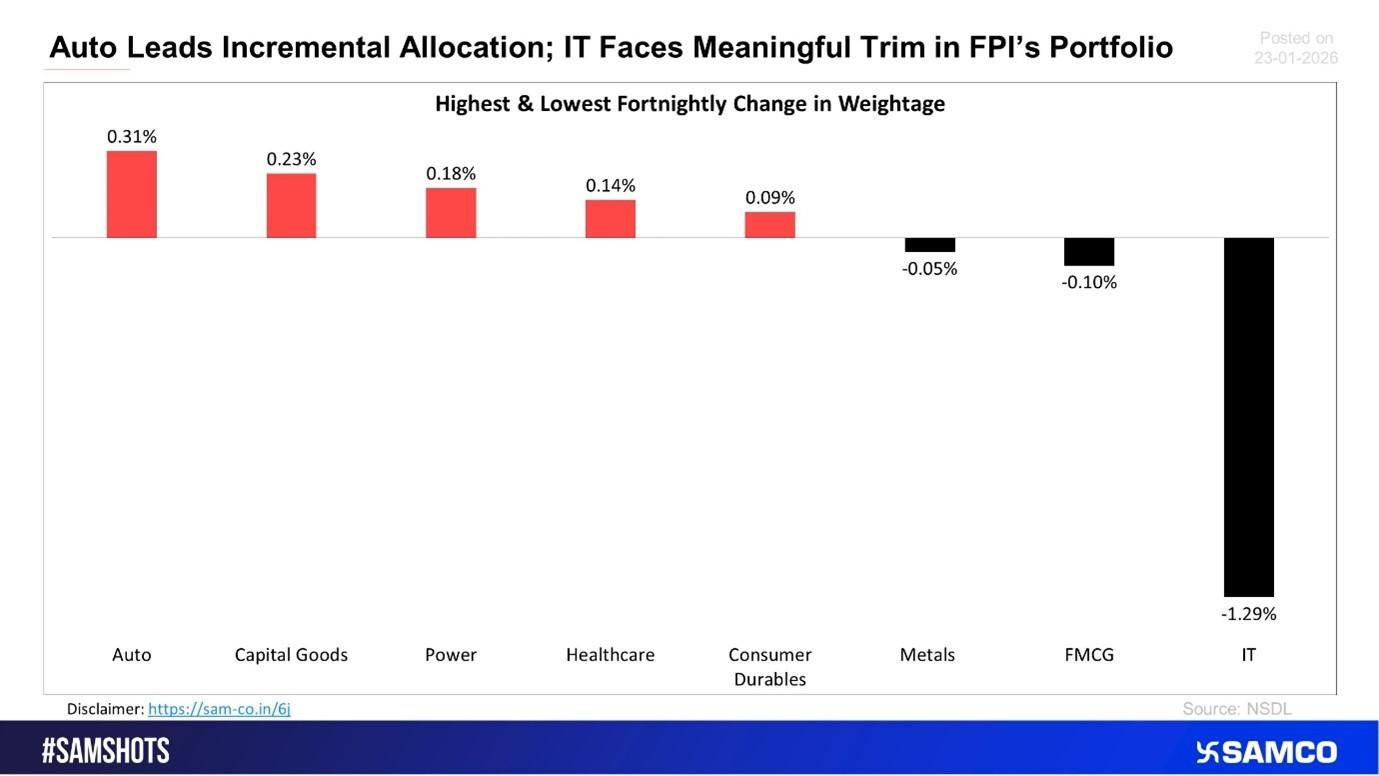

Sector Weightage Changes: Where FPIs Increased Exposure

The change in portfolio weight further confirms the tactical repositioning.

Top Weight Gainers

- Auto: +0.31%

- Capital Goods: +0.23%

- Power: +0.18%

- Healthcare: +0.14%

- Consumer Durables: +0.09%

Top Weight Losers

- IT: -1.29%

- FMCG: -0.10%

- Metals: -0.05%

The rise in Auto and Capital Goods reinforces the domestic consumption and investment cycle theme.

What This Means for Investors?

The February FPI trend highlights three key market signals:

1. Domestic Growth is the Core Theme

Sectors linked to infrastructure, manufacturing, financials, and consumption are gaining institutional attention.

2. Capex Cycle Confidence is Rising

Heavy inflows into Capital Goods, Power, and Construction indicate strong conviction in India’s multi-year investment cycle.

3. Export-Oriented Sectors Face Near-Term Pressure

IT and other globally exposed sectors may remain volatile due to demand uncertainties and portfolio rebalancing.

Outlook: Tactical Rotation, Not Structural Exit

While the selling in IT and defensives appears significant, the broader trend suggests tactical reallocation rather than structural exits. FPIs are repositioning portfolios to align with:

- India’s domestic growth momentum

- Infrastructure expansion

- Credit and investment cycle recovery

If the macro environment remains supportive, domestic cyclicals and capex-linked sectors could continue to attract institutional flows in the near term.

Conclusion

The first half of February 2026 clearly reflects a strategic shift in FPI positioning. With net inflows of Rs 19,675 crore, institutional investors are increasingly favoring Capital Goods, Financials, Power, and other domestic growth sectors, while trimming exposure to IT, FMCG, and other defensive segments.

For market participants, tracking such sectoral rotations can provide early signals of emerging investment themes and institutional conviction in India’s economic growth story.

Easy & quick

Easy & quick

Leave A Comment?