The Indian stock market witnessed notable volatility in auto and auto ancillary stocks following headlines around the India–EU auto trade agreement. Several Nifty Auto constituents corrected sharply in January, prompting concerns about rising import competition and margin pressure on domestic manufacturers.

However, a deeper analysis suggests the market reaction is disproportionate to the deal's actual economic impact. Structural safeguards within the agreement significantly limit near-term disruption to India’s automobile industry.

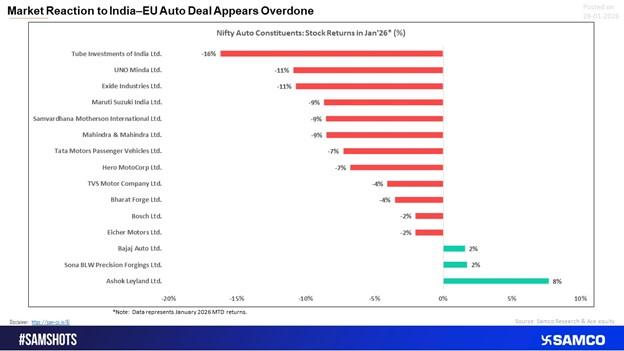

Market Reaction: Sentiment Outpaces Fundamentals

Auto stocks underperformed in January amid fears of cheaper European imports entering the Indian market. Stocks across OEMs and auto component manufacturers saw declines despite no immediate change in operating conditions.

This sell-off appears to be sentiment-led rather than fundamentals-driven, as the trade agreement’s design restricts both the scale and speed of tariff benefits.

Why the Impact of the India–EU Auto Deal Remains Limited

1. Import Quota Caps the Addressable Market

The agreement allows tariff benefits on a maximum of 250,000 vehicles per year, which translates to only 6–7% of India’s ~4 million passenger vehicle market. This quota sharply limits the number of vehicles that can enter India at reduced duties, preventing any large-scale disruption to domestic players.

2. Mass-Market Vehicles Remain Fully Protected

Cars priced below ₹25 lakh, which form the backbone of India’s passenger vehicle sales, are excluded from tariff concessions. Since the bulk of domestic OEM volumes lie in this segment, competitive pressure from imports remains minimal.

3. Electric Vehicle Imports Deferred for Five Years

Battery electric vehicles (EVs) do not receive tariff reductions for the first five years of the agreement. Any relief is phased in gradually thereafter, providing domestic EV manufacturers ample time to scale production, localise supply chains, and improve cost competitiveness.

4. Luxury Automakers Already Manufacture Locally

More than 90–95% of European luxury vehicle sales in India are already assembled locally through CKD and SKD routes. As a result, the scope for incremental gains from duty cuts on fully built units (CBUs) is limited.

This significantly reduces the likelihood of aggressive pricing by European OEMs in the Indian market.

5. Phased Implementation Restricts Near-Term Benefits

The agreement follows a gradual, quota-bound rollout, limiting immediate benefits for importers. Additionally, factors such as currency fluctuations, GST, cess, and local taxes may dilute the benefit of lower customs duties, keeping effective landed costs elevated.

What the Data Indicates

Despite the structural limitations, Nifty Auto constituents recorded negative returns in January, reflecting fear of future competition rather than near-term earnings risk. Historically, such headline-driven corrections have often created selective opportunities in fundamentally strong auto stocks.

Outlook for Indian Auto Stocks

From an industry perspective, the India–EU auto trade deal:

- Does not threaten mass-market OEMs

- Has a limited impact on near-term profitability

- Protects the domestic EV ecosystem

- Favours players with strong localisation and scale

Unless the agreement undergoes material expansion in quotas or pricing thresholds, its impact is likely to remain incremental rather than disruptive.

Investor Takeaway

The sharp correction in auto stocks appears overdone relative to the actual scope of the India–EU auto trade agreement. Structural safeguards, phased execution, and strong domestic manufacturing capabilities act as effective buffers for Indian automakers.

For long-term investors, the recent volatility may represent a sentiment-driven adjustment rather than a structural downturn, particularly for companies with strong domestic demand visibility.

Easy & quick

Easy & quick

Leave A Comment?