India’s retail auto market in November 2025 reflected steady demand, subtle market-share shifts, and continued traction for EV-led OEMs. Here’s a detailed breakdown of performance across the 2W, 3W, PV, and CV segments, based on OEM retail market shares.

Two-Wheeler (2W) Market Share Highlights – November 2025

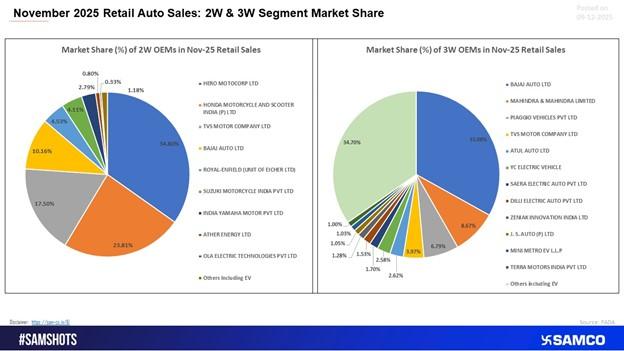

The two-wheeler segment maintained stable momentum, though competitive shifts were visible among the top players.

Key Takeaways

- Hero MotoCorp remained the industry leader with a 34.8% market share, marginally lower YoY as rural recovery remained uneven.

- Honda Motorcycle and Scooter India (HMSI) held the second position at 23.8%, but posted the sharpest YoY decline due to softer scooter volumes.

- TVS Motor Company delivered one of the strongest performances, gaining share to 17.5%, supported by scooters, premium motorcycles, and its expanding EV lineup.

- Bajaj Auto slipped to 10.2%, impacted by softer domestic motorcycle demand.

- Royal Enfield improved its share to 4.5%, benefitting from a recovery in mid-premium motorcycle demand and new model launches.

- EV-focused OEMs such as Ather continued to show incremental gains, reflecting rapid electrification in urban markets.

Three-Wheeler (3W) Market Share Highlights – November 2025

Momentum in the three-wheeler segment remained strong, supported by rising EV penetration, urban mobility demand, and strong cargo adoption.

Key Takeaways

- Bajaj Auto maintained category dominance with a 33% market share, though slightly lower YoY.

- Mahindra & Mahindra gained traction, rising to 8.7%, driven by strong EV passenger carrier sales.

- Piaggio Vehicles saw its share soften to 6.8%, pressured by competitive pricing and rising EV substitution.

- TVS Motor nearly doubled its share to 4%, driven by growth in electric rickshaws and compact cargo 3Ws.

- Emerging EV-only OEMs recorded meaningful share gains, indicating a structural market shift toward electrification.

Passenger Vehicles (PV) Market Share Highlights – November 2025

The passenger vehicle market remained robust with SUVs, hybrids, and EVs driving significant consumer demand.

Key Takeaways

- Maruti Suzuki continued to dominate with a 39.4% market share, supported by strong demand in entry, hatchback, and compact SUV segments.

- Mahindra strengthened further, rising to 13.7%, benefiting from sustained SUV momentum.

- Tata Motors held 13.2%, supported by premium SUVs and strong EV traction.

- Hyundai’s share moderated to 12.6%, impacted by heightened competition in the mid-SUV category.

- Toyota posted marginal gains, driven by hybrids, MPVs, and its premium SUV lineup.

Commercial Vehicles (CV) Market Share Highlights – November 2025

The commercial vehicle segment remained healthy, supported by infrastructure spending, fleet replacement cycles, and festive dispatches.

Key Takeaways

- Tata Motors sustained leadership at 35.1%, though slightly softer YoY.

- Mahindra improved to 29.7%, driven by strong performance in the LCV (Light Commercial Vehicle) category.

- Ashok Leyland remained stable at 16.2%, supported by steady M&HCV demand.

- VE Commercial Vehicles (VECV) improved to 7.5%, benefitting from strong demand in heavy-duty trucks.

- Market share distribution remained largely stable, indicating balanced demand across segments.

Overall Market View

The auto sector in November 2025 showed:

- Stable retail performance across categories

- Gradual market share shifts driven by EV penetration

- Strong demand for SUVs, premium bikes, EV scooters, and 3W passenger carriers

- Consistent CV momentum supported by infrastructure activity

The month highlights ongoing structural changes, particularly EV adoption, rising preference for premium products, and sustained dominance of leading OEMs across segments.

Easy & quick

Easy & quick

Leave A Comment?