Introduction

Options trading in India has evolved from being a niche segment to one of the most actively traded derivatives markets globally. With the rise in retail participation, understanding Options Greeks—the metrics that measure different dimensions of risk—has become essential. Among these Greeks, Gamma plays a crucial role in determining how sensitive an option’s Delta is to movements in the underlying asset, such as the Nifty 50 or Bank Nifty index.

For Futures & Options (F&O) traders, mastering Gamma can be the difference between strategic precision and unexpected losses. It helps traders anticipate how their position’s risk profile changes with volatility and price fluctuations.

To simplify this complex concept, tools like the Samco trading app offer real-time analytics that factor in Gamma and other Greeks, empowering traders to make data-driven decisions and strengthen their options trading strategies.

What Is Gamma?

In options trading, Gamma measures the rate of change of Delta in response to a ₹1 change in the underlying asset’s price. While Delta tells you how much an option’s price moves relative to the underlying, Gamma reveals how quickly Delta itself changes. It’s often referred to as the second derivative of the option’s price concerning the underlying’s price.

For instance, suppose you hold a Nifty 50 call option with a Delta of 0.50. This means if Nifty rises by ₹1, the option’s premium will increase by ₹0.50. However, if Gamma is 0.05, then for every ₹1 increase in Nifty, the Delta will rise by 0.05. So, after the ₹1 move, your Delta becomes 0.55—indicating higher sensitivity to further price increases.

Gamma is highest for at-the-money (ATM) options and declines as options move in-the-money (ITM) or out-of-the-money (OTM). It’s a crucial component for active traders, especially when managing short-term positions, as it influences how rapidly risk exposure shifts with market moves.

In simple terms, while Delta tells you how much your option might gain or lose, Gamma tells you how fast that change accelerates. Understanding this acceleration allows traders to manage risk dynamically—especially when dealing with volatile assets or during major market events like RBI policy announcements or budget sessions.

Why Are F&O Traders Losing Money?

Despite the explosive growth of the Indian F&O market, a large number of traders continue to lose money. According to SEBI’s 2023 report, nearly 9 out of 10 individual traders in the F&O segment incur net losses. One significant reason is the lack of understanding of the options Greeks, particularly Gamma.

Most traders focus solely on price direction—buying calls when bullish or puts when bearish—without realizing how Delta and Gamma interact. When volatility spikes, Gamma can cause Delta to change drastically, making even well-intentioned trades go wrong. For instance, a short call position with high Gamma exposure can result in mounting losses as prices move quickly against the trader.

Another frequent mistake is inadequate strike price selection. Many retail traders pick deep OTM options because they appear cheaper, ignoring that these options have low Gamma, meaning they respond minimally to favorable price moves. Conversely, professional traders prefer ATM or slightly ITM strikes, where Gamma is more responsive, allowing better control over position adjustments.

Lack of risk management further compounds the issue. Traders fail to hedge positions or rebalance when Gamma exposure increases. A sudden 200-point move in Nifty Futures (with a lot size of 75) can drastically alter portfolio sensitivity—turning a seemingly small position into a large directional bet.

In summary, understanding and managing Gamma helps traders anticipate how their portfolio’s Delta will evolve as the market moves. Ignoring it is akin to driving a car without realizing how fast it can accelerate—until it’s too late.

Factors Influencing Gamma

Gamma is not constant—it fluctuates with several market variables. Understanding these factors helps traders anticipate changes in option sensitivity and better manage risk. The three most influential factors are:

- a) Moneyness of the Option

Gamma is highest for at-the-money (ATM) options, where small moves in the underlying asset can significantly change the Delta. For example, if Nifty is trading at ₹25,000, the 25,000 strike call or put will have the highest Gamma. In contrast, in-the-money (ITM) or out-of-the-money (OTM) options exhibit lower Gamma since their Deltas are already near 1 or 0, meaning they respond less dynamically to price movements.

- b) Time to Expiration

As expiry nears, Gamma for ATM options increases sharply, creating what traders call “Gamma spikes.” This means that even a small move in Nifty near expiry can cause large swings in Delta, and hence in option prices. Traders often see this during weekly expiries on the NSE—when Thursday volatility leads to sudden surges or crashes in option premiums. Longer-dated options, on the other hand, exhibit smoother Gamma behavior.

- c) Volatility of the Underlying

Gamma tends to be higher in low-volatility environments and lower when implied volatility (IV) is high. This might sound counterintuitive, but when IV rises, option premiums expand, flattening Gamma’s curve. In calm markets, Gamma becomes more pronounced since option prices are more sensitive to small moves.

- d) Practical Implication

Consider a trader holding one Nifty ATM call with Gamma of 0.08. A 100-point rise in Nifty (₹25,000 to ₹25,100) would increase the Delta by 0.08 × 100 = 8 points per unit. For a 75-lot position, this equates to 8 × 75 = ₹600 per point in exposure change—illustrating how even small shifts in Gamma can alter the position’s behavior significantly.

Understanding these drivers allows traders to anticipate when Gamma risk will rise, enabling better hedging and strike selection strategies.

How to Select the Right Strike Price in Options Trading

Choosing the right strike price is one of the most critical decisions in options trading, and Gamma can be a valuable guide here. The strike you select defines how responsive your option will be to market movements.

- At-the-Money (ATM) Strikes:

These have the highest Gamma and are ideal for short-term directional traders who seek quick responses to price changes. For instance, if Nifty is at ₹25,000, a 25,000 Call will have the highest Gamma, making it most reactive to a ₹50–₹100 move. - In-the-Money (ITM) Strikes:

ITM options have moderate Gamma but higher Delta. They are better suited for traders with stronger conviction, as these options move more linearly with the underlying. - Out-of-the-Money (OTM) Strikes:

These have low Gamma, which means their Delta changes slowly. Though cheaper, they are less responsive and often expire worthless unless the underlying moves sharply.

For example, if a trader buys a Nifty 25,000 Call (ATM) with Gamma 0.06 and Delta 0.50, a 100-point move could raise Delta to 0.56. This higher Delta increases the option’s sensitivity, amplifying potential returns (and risks).

Gamma also helps traders balance risk vs. reward—a high Gamma offers quick profits but requires active management, while low Gamma offers stability but slower payoffs.

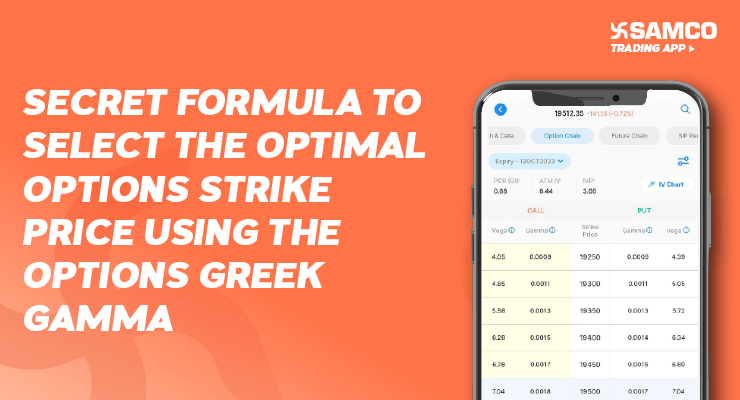

Using the Samco trading app, traders can visualize Gamma alongside Delta and Vega for each strike, helping select the optimal balance between risk exposure and market responsiveness.

F&O Strategies with Options Greeks

Incorporating Gamma into trading strategies allows traders to manage risk dynamically and profit from volatility. Two key strategies stand out in the Indian F&O context:

- a) Gamma Scalping

Gamma scalping involves holding a Delta-neutral position (where overall Delta ≈ 0) and profiting from price swings in the underlying asset. A trader typically buys an ATM option (high Gamma) and hedges Delta exposure by selling Nifty Futures.

For example, if Nifty trades at ₹25,000, a trader may buy one 25,000 Call (Gamma = 0.07) and short Nifty Futures. As Nifty rises, Delta increases, and the trader sells Futures to stay hedged—locking in small profits. As Nifty falls, the trader buys back Futures at lower prices, again profiting.

This strategy works best in volatile, range-bound markets, like the weekly expiry scenarios on NSE, where frequent rebalancing captures time-decay and volatility shifts.

- b) Delta–Gamma Neutral Strategy

Institutional traders often combine Delta and Gamma hedging to minimize directional risk. A Delta–Gamma neutral position ensures that both the first and second-order price sensitivities are neutralized.

For instance, a portfolio of Nifty and Bank Nifty options may be structured so that changes in Delta from price movements are offset by Gamma exposure in other options. This is typically achieved using a combination of Calls and Puts across multiple strike prices.

These strategies, while complex, highlight Gamma’s importance in active F&O portfolio management. They enable traders to respond swiftly to market changes, rather than reacting after losses accumulate.

With modern tools like the Samco trading app, traders can simulate such strategies, monitor live Greeks, and visualize how small price or volatility shifts affect their positions—an advantage that previously only institutional traders enjoyed.

Using the Samco Trading App to Factor in Gamma

The Samco trading app provides advanced analytics designed for retail and professional F&O traders alike. It allows users to visualize and manage their exposure to Greeks, including Gamma, in real-time.

Step-by-Step Guide to Using Gamma Insights on Samco:

- Open the Derivatives Analytics Dashboard – Select your Nifty or Bank Nifty option contract.

- View Greeks Breakdown – The platform displays Delta, Gamma, Vega, Theta, and Rho for each strike.

- Assess Gamma Exposure – Identify which of your positions have high Gamma and how this may change near expiry.

- Scenario Analysis – Use Samco’s real-time simulation tool to project how a ₹100 or ₹200 move in Nifty affects your portfolio’s Greeks.

- Adjust or Hedge Accordingly – Based on Gamma readings, rebalance using Futures or options at different strikes to maintain desired exposure.

Samco’s in-built options Greeks calculator automatically factors in parameters like implied volatility, time to expiry, and lot size (e.g., Nifty = 75 units, Bank Nifty = 15 units) to deliver precise results.

This empowers traders to make informed decisions rather than guessing market moves. By factoring in Gamma, users can better anticipate when their Delta exposure might accelerate—helping manage risks and capture opportunities efficiently.

Improving Your F&O Strategies with Gamma

To truly excel in options trading, Gamma must be integrated into every decision—from strike selection to position sizing and hedging. Here are a few best practices for improving your strategy:

- Monitor Gamma Exposure Regularly: As expiry approaches, Gamma risk spikes—requiring tighter monitoring and quicker rebalancing.

- Use Gamma to Time Entries and Exits: When Gamma is high, even small moves can yield significant changes in P&L. Use it to identify high-potential intraday opportunities.

- Combine Gamma with Other Greeks: Integrating Delta, Vega, and Theta insights ensures a complete view of position sensitivity.

- Leverage Analytics Tools: Apps like Samco’s provide real-time Gamma analytics—something even experienced traders find invaluable for precise risk control.

Continuous learning, simulation, and disciplined use of data-driven tools will enable traders to navigate the fast-paced Indian F&O markets more confidently and profitably.

Conclusion

In the dynamic world of options trading, Gamma acts as the accelerator of risk and reward. It helps traders understand how quickly their exposure changes, enabling smarter, faster, and more controlled decisions.

By incorporating Gamma into F&O strategies—especially with the analytical power of the Samco trading app—traders can elevate their performance from reactive to proactive. Whether you trade Nifty, Bank Nifty, or stock options, mastering Gamma isn’t just an advantage—it’s a necessity for long-term success.

Start analyzing your Gamma exposure today and elevate your options trading strategy with data-driven precision.

Easy & quick

Easy & quick

Leave A Comment?