Vedanta Limited, one of India’s most diversified natural resources conglomerates, continues to derive strength from its multi-segment business model. The company’s portfolio spans oil & gas, aluminium, iron & steel, power, and a broad ‘other’ category, each contributing uniquely to its revenue mix, profitability, and valuation framework. The latest segmental data highlights where the company’s earnings power lies—and where potential value unlocking may emerge.

Aluminium: The Core Earnings Driver

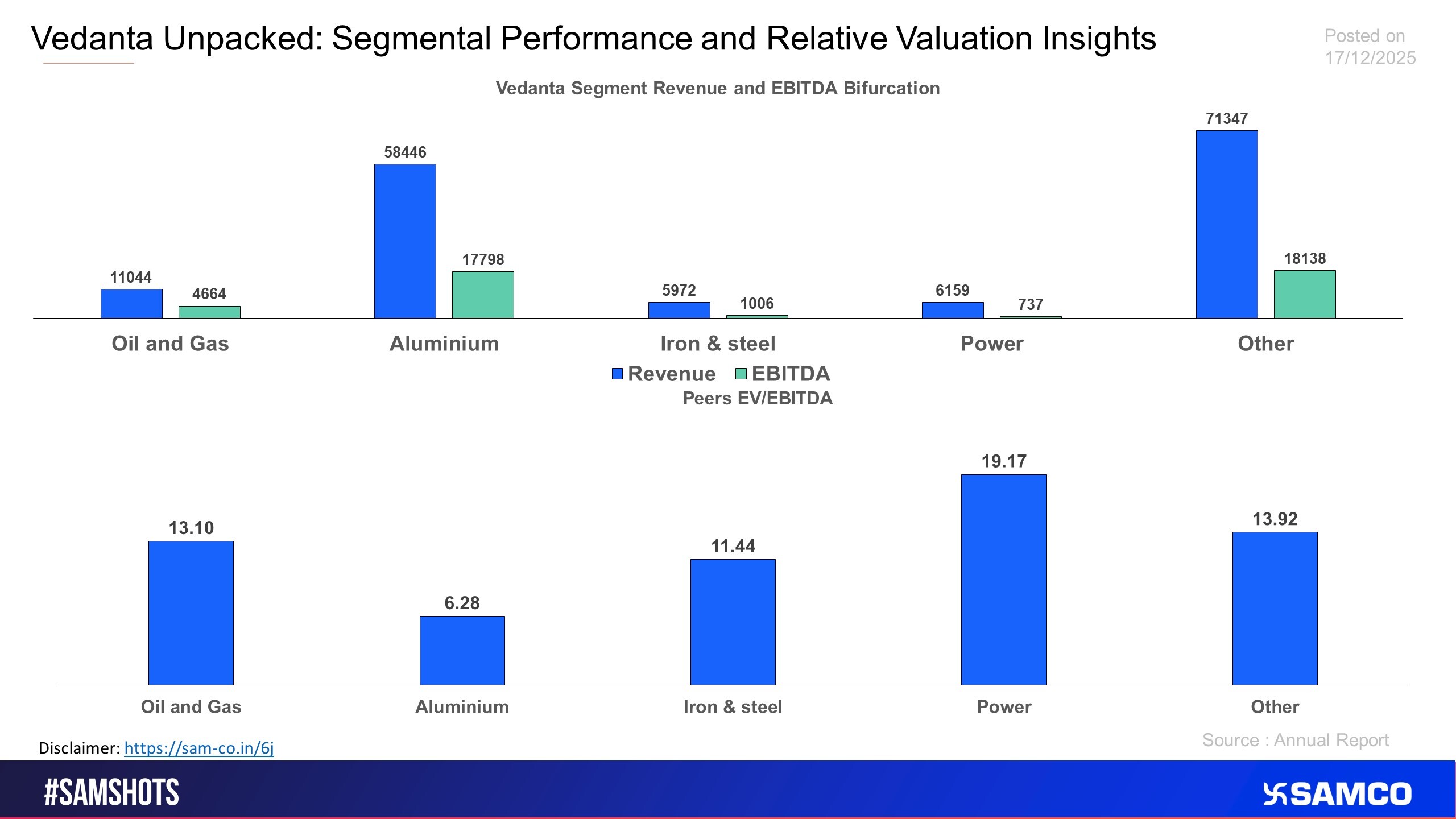

Vedanta’s Aluminium segment remains its most significant business by scale, generating

- ₹58,446 crore in revenue, and

- ₹17,798 crore in EBITDA.

Despite being capital-intensive, the segment trades at a relatively low peer EV/EBITDA multiple of 6.28x. This indicates valuation comfort, especially given Vedanta’s integrated operations, improving cost efficiencies, and long-term demand outlook driven by energy transition and infrastructure spending.

Oil & Gas: Strong Margins and Cash Flow Stability

The Oil & Gas division delivered:

- ₹11,044 crore in revenue, and

- ₹4,664 crore in EBITDA.

With a peer multiple of 13.10x EV/EBITDA, the segment commands a premium, reflecting its robust margins, predictable cash flows, and strategic relevance in India’s energy requirements. Stable crude production and ongoing field development continue to support this business.

Iron & Steel: Smaller but Supported by Cyclical Tailwinds

Vedanta’s Iron & Steel business contributed:

- ₹5,972 crore in revenue, and

- ₹1,006 crore in EBITDA.

Peer valuations at 11.44x EV/EBITDA signal market expectations of a cyclical recovery in the steel sector. While smaller in scale for Vedanta, the segment benefits from rising domestic steel demand and productivity-focused improvements.

Power: Defensive and Regulated Business

The Power vertical posted:

- ₹6,159 crore in revenue, and

- ₹737 crore in EBITDA,

with a high peer valuation of 19.17x EV/EBITDA. This elevated multiple reflects the defensive nature of power assets, regulated returns, and their importance in supporting Vedanta’s energy-intensive operations.

Other Businesses: Diversified Growth and Optionality

Vedanta’s Other segment remains a strong contributor with:

- ₹71,347 crore in revenue, and

- ₹18,138 crore in EBITDA.

It trades at 13.92x EV/EBITDA, highlighting a blend of stable earnings and future optionality across diversified verticals such as zinc, copper, and other resources.

Conclusion: Value-Unlocking Opportunity Across Segments

Vedanta’s broad earnings mix, coupled with diverse peer valuation multiples, reveals an interesting landscape for investors. Capital-heavy businesses like aluminium offer valuation comfort, while segments such as oil & gas and power command premium multiples due to stability and steady cash flows.

The company’s diversified structure provides both resilience and potential for value unlocking, especially as demand cycles evolve across commodities.

Easy & quick

Easy & quick

Leave A Comment?