The Indian automobile industry ended December 2025 on a strong note, sealing a solid Q3 FY26 performance across key segments. Data from two-wheelers (2W), passenger vehicles (PV), and commercial vehicles (CV) highlights a clear consumption-led recovery, supported by favourable macro conditions, festive demand, and policy support.

Strong Momentum in Two-Wheelers

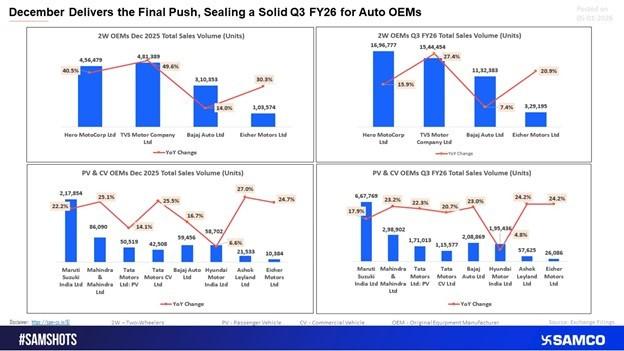

The two-wheeler segment continued to demonstrate resilience and growth during both December 2025 and Q3 FY26. Hero MotoCorp and TVS Motor Company emerged as clear leaders, reporting robust year-on-year growth on a monthly as well as quarterly basis. Improved affordability, easing input costs, and sustained rural demand played a key role in driving volumes.

Premium-focused players were not left behind. Eicher Motors recorded steady traction, indicating that discretionary spending in higher-end motorcycle segments remains intact despite past volatility.

Passenger Vehicles Maintain Growth Trajectory

The passenger vehicle segment remained a major growth engine for the industry. Maruti Suzuki India and Mahindra & Mahindra continued to anchor volumes, benefiting from strong order books, new product launches, and consistent consumer demand.

SUV-led growth, better availability of semiconductors, and improved financing conditions supported sustained momentum through the quarter. PV volumes reflect increasing consumer confidence and a gradual normalization of urban and semi-urban demand patterns.

Commercial Vehicles Show Gradual Recovery

Commercial vehicle sales continued their measured but steady recovery, with Tata Motors and Ashok Leyland reporting improving volumes. Rising fleet utilisation, infrastructure-led spending, and a pick-up in freight activity contributed to better performance, particularly in the medium and heavy CV segments.

While CVs are still trailing pre-cycle peaks, the sequential improvement suggests that the sector is on a firmer footing.

Policy Support and Macro Tailwinds Drive Demand

Q3 FY26 benefitted from several supportive macro and policy developments. GST rationalisation implemented in September provided relief to the sector, followed by strong festive and wedding-season demand. Additionally, the RBI’s rate cut in December improved sentiment and boosted vehicle financing demand across segments.

Together, these factors translated into improved showroom footfalls, better conversion rates, and higher dispatches by OEMs.

Outlook: Constructive Near-Term View for Auto Sector

Overall, December 2025 and Q3 FY26 data indicate that macroeconomic stability and policy support are translating into real, broad-based auto demand. Strength across two-wheelers and passenger vehicles, combined with improving commercial vehicle utilisation, reinforces a constructive near-term outlook for the Indian automobile sector.

With easing inflation, improving rural incomes, and supportive credit conditions, the auto industry appears well-positioned to sustain momentum into the coming quarters.

Easy & quick

Easy & quick

Leave A Comment?