Premium consumer stocks drew fresh FPI inflows in Q1 FY26, while several large-cap staples faced outflows, signaling a rotation toward higher-margin, brand-led franchises and niche categories amid a mixed consumption backdrop. This pattern aligns with 2025 sector flow data showing FPIs trimming FMCG exposure overall, even as select premium names benefited from stock-specific earnings strength and premiumization narratives.

Why premium led

- Stronger earnings and pricing power in premium brands improved confidence, with Marico highlighting double‑digit revenue growth and robust margins around Q1 FY26, supporting renewed foreign interest at elevated share prices.

- FPIs have been rotating away from defensives like FMCG at the sector level, yet selectively adding exposure to quality consumer names where brand strength and execution drive profitability.

What the flows show

- Sector snapshots from mid‑2025 indicate sizable net FPI outflows from FMCG overall, even as the “smart money” reallocated within consumption toward higher‑growth, premium, and discretionary adjacencies.

- This selective stance mirrors on‑ground demand data: rural volumes still outpace urban but are slowing, with consumers shifting to more miniature packs, pressuring mass‑market volume leverage for staples.

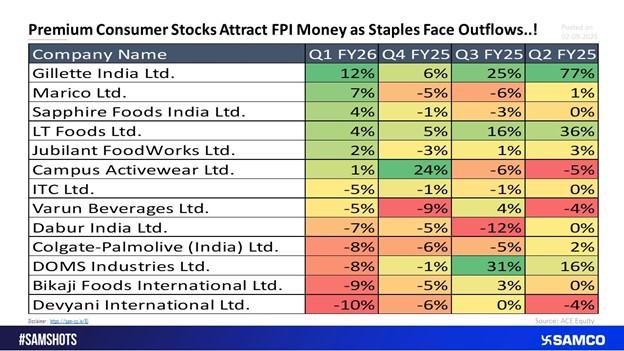

Company highlights

- Gillette India: Grooming’s premium positioning aligns with FPI preference for brand moats and margin resilience in consumer categories.

- Marico: Stock at or near record highs alongside Q1 FY26 momentum and efficient operations helped reverse prior FPI outflows, signaling renewed conviction in fundamentals.

- Sapphire Foods and LT Foods: Niche categories with improving flow trends benefited from discretionary recovery pockets and export/premiumization angles.

- ITC, Dabur, Colgate-Palmolive: Continued trimming reflects caution on mass‑staples volume growth as rural normalization moderates and consumers favor lower unit packs.

Macro demand signals

- NielsenIQ’s latest reads show FMCG volume growth slowed to 5.1% in Q1 2025, with rural growth decelerating but still outperforming urban; the mix shift toward small packs underscores value-seeking behavior.

- Corporate commentaries through mid‑2025 echoed a gradual demand recovery path, with premium and non‑food segments leading while broad staples volumes remained uneven.

Investment takeaways

- Prefer category leaders with clear moats: Pricing power, premium mix, and distribution depth are key to sustaining earnings in a mixed macro and capturing future FPI interest.

- Balance defensiveness with growth: While staples provide stability, the current flow regime rewards premiumization and discretionary‑adjacent earnings visibility.

- Track rural trajectory and pack‑price architecture: A firmer rural upcycle could rebalance flows back to mass staples; persistent small‑pack skew favors premium names with flexible pack-price strategies.

Easy & quick

Easy & quick

Leave A Comment?