In this article, we will discuss

- What Are Strategy Legs In Risk Reversal Strategy?

- What Will Be The Payoff Of The Strategy?

- Who Can Deploy This Strategy?

- When Should This Strategy Be Deployed?

- Understanding Strategy Greeks

- Things to Keep In Mind

- Conclusion

Risk reversal is a type of option strategy that involves buying a put option and selling a call option on the same underlying asset with the same expiration date. This strategy is used to hedge a short position in the underlying asset or to speculate on a downward price movement.

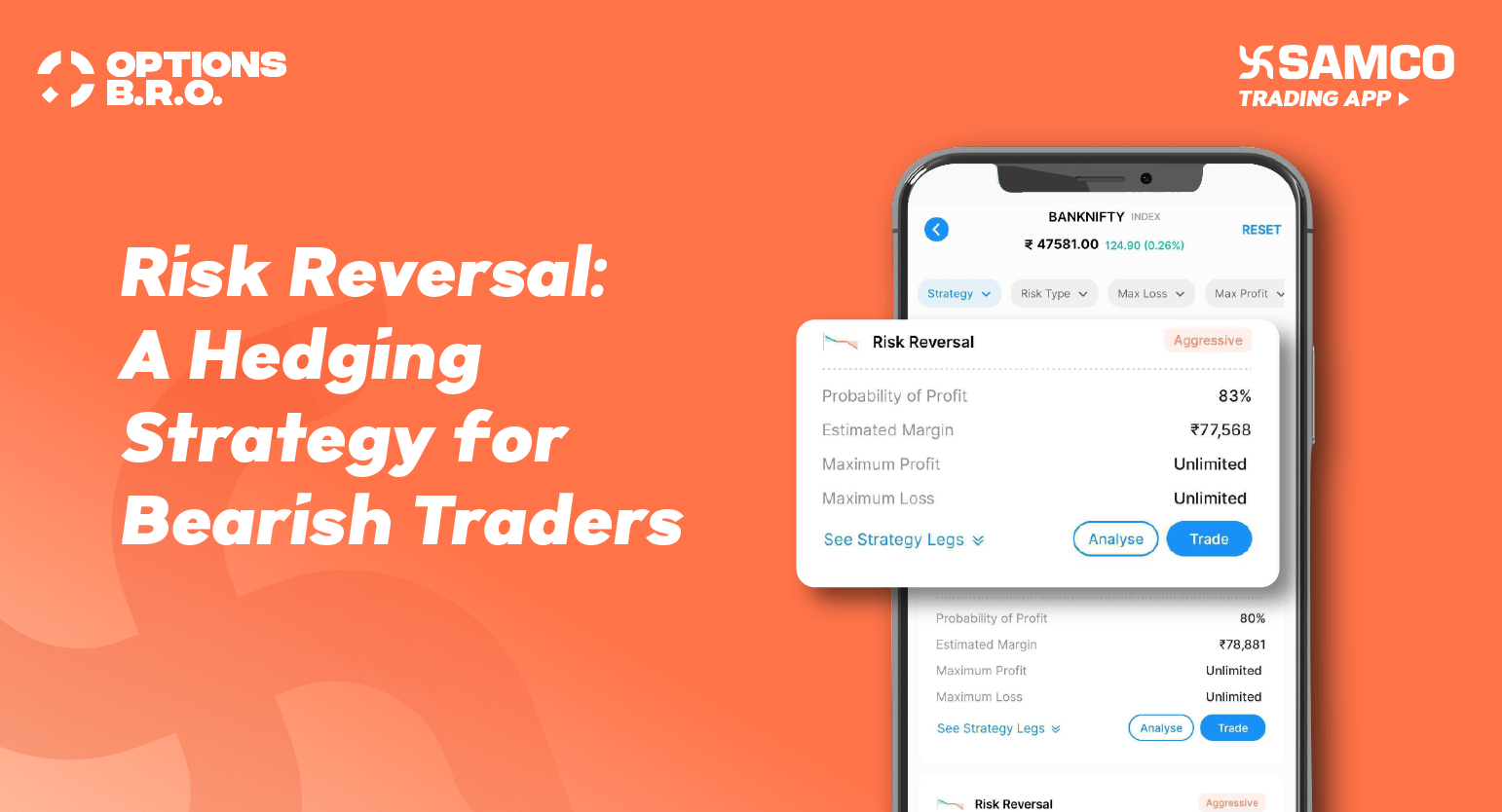

To implement a risk reversal strategy effectively, you need the right tools at your disposal. Samco Securities offers a wide range of advanced tools for options traders who want to improve their trading performance. The best part? These tools are available free of cost for Samco users on the Samco Trading App — like options Greeks, Options B.R.O, options chains and more.

What Are Strategy Legs In Risk Reversal Strategy?

In a risk reversal strategy, you buy one out-of-the-money (OTM) put option and sell one OTM call option. The strike price of the call option and the put option should be equidistant from the at-the-money (ATM) strike price. For example, if the current price of a stock is ₹ 100, you can buy a put option with a strike price of ₹ 90 and sell a call option with a strike price of ₹ 110. Both options should have the same expiration date, say one month from now.

The put option gives you the right, but not the obligation, to sell the underlying asset at the strike price before or on the expiration date. The call option gives the buyer the right, but not the obligation, to buy the underlying asset at the strike price before or on the expiration date. By selling the call option, you receive a premium from the buyer, which reduces the cost of buying the put option. However, by selling the call option, you also give up the potential upside of the underlying asset above the strike price.

What Will Be The Payoff Of The Strategy?

The payoff of the risk reversal strategy depends on the price of the underlying asset at the expiration date. There are three possible scenarios:

- If the price of the underlying asset is below the strike price of the put option, you will exercise the put option and sell the underlying asset at the strike price. You will also let the call option expire worthless. Your profit will be the difference between the strike price of the put option and the price of the underlying asset, minus the net premium paid or received for the options. Your profit will increase as the price of the underlying asset decreases.

- If the price of the underlying asset is between the strike prices of the call and put options, you will let both options expire worthless. Your profit or loss will be equal to the net premium paid or received for the options. Your profit or loss will be minimal and will not be affected by the price of the underlying asset.

- If the price of the underlying asset is above the strike price of the call option, you will be assigned to the call option and have to sell the underlying asset at the strike price. You will also let the put option expire worthless. Your loss will be the difference between the strike price of the call option and the price of the underlying asset. Plus/minus will depend on whether the net premium is paid or received for the options.

The following table summarises the payoff of the risk reversal strategy:

| Price of Underlying Asset | Payoff of Put Option | Payoff of Call Option | Net Payoff of Risk Reversal |

|---|---|---|---|

| Below put strike price | Strike price - Price | 0 | Strike price - Price - Net premium |

| Between put and call strike prices | 0 | 0 | Net premium |

| Above call strike price | 0 | Price - Strike price | Price - Strike price + Net premium |

Who Can Deploy This Strategy?

This strategy can be deployed by traders who have a bearish view on the underlying asset and want to hedge their short position or speculate on a downward price movement. This strategy is suitable for traders who have an aggressive approach and are willing to take unlimited risk on the upside. Since this strategy involves selling a call option, the trader needs to have enough margin in their account to cover the potential loss.

When Should This Strategy Be Deployed?

This strategy should be deployed when the trader expects the price of the underlying asset to fall significantly in the near future and does not want to take any risk of theta or vega. Theta is the rate of change of the option value with respect to time. Vega is the rate of change of the option value with respect to volatility. If the trader buys a put option alone, they will have to pay a high premium and will lose money if the price of the underlying asset does not move enough or if the volatility decreases. By selling a call option, the trader can reduce the cost of the put option or even receive a net credit. The trader can also benefit from the decrease in volatility, as it will lower the value of the call option more than the put option.

Understanding Strategy Greeks

Greeks are the measures of the sensitivity of the option value to various factors, such as price, time, volatility, and interest rate. The main greeks that affect the risk reversal strategy are delta, gamma, theta, and vega.

- Delta is the rate of change of the option value with respect to the price of the underlying asset. Delta of the strategy will depend on the selected strike prices. If the selected strike prices are very far from the ATM strike price, delta will be very low, meaning the option value will not change much with the price of the underlying asset.

- Gamma is the rate of change of the delta with respect to the price of the underlying asset. Gamma will play a major role in this strategy, as it will affect the rate of change of the option value with the price of the underlying asset.

- Theta is the rate of change of the option value with respect to time. Theta will play a very minimal role in this strategy, as the call and put options will neutralise the theta of each other. The theta of the call option will be negative, as it will lose value with time.

- Vega is the rate of change of the option value with respect to volatility. Vega will also play a very minimal role in this strategy, as the call and put options will neutralise the vega of each other. The vega of the call option will be positive, as it will gain value with volatility. The vega of the put option will be negative, as it will lose value with volatility. The net vega of the risk reversal strategy will be close to zero, as the vega of the call option will cancel out the vega of the put option.

Things to Keep In Mind

In this strategy, managing the risk is very difficult if the view goes wrong. The trader faces unlimited risk on the upside, as the call option can be exercised at any price above the strike price. The trader also faces the risk of margin call, as the broker may require additional funds to cover the potential loss. Therefore, it is better to maintain a strict stop loss based on the resistance level of the underlying asset. The trader should also monitor the price movement and the implied volatility of the options and adjust the strategy accordingly.

Conclusion

Risk reversal strategy can be applied to any underlying asset that has liquid options available, such as stocks, indices, commodities, or currencies. Some of the popular underlying assets for risk reversal strategy are Nifty 50, Bank Nifty, Reliance Industries, HDFC Bank, Tata Motors, etc. The trader can choose the strike prices and the expiration dates of the options based on their view and risk appetite. For this use, Options B.R.O. . Options B.R.O. is a feature in the Samco trading app that helps options traders to build, research, and optimise their trading strategies. Options B.R.O. uses cutting-edge analytical procedures and technical indicators to filter and rank the best options strategies for the traders based on their inputs.

Disclaimer: INVESTMENT IN SECURITIES MARKET ARE SUBJECT TO MARKET RISKS, READ ALL THE RELATED DOCUMENTS CAREFULLY BEFORE INVESTING. The asset classes and securities quoted in the film are exemplary and are not recommendatory. SAMCO Securities Limited (Formerly known as Samruddhi Stock Brokers Limited): BSE: 935 | NSE: 12135 | MSEI- 31600 | SEBI Reg. No.: INZ000002535 | AMFI Reg. No. 120121 | Depository Participant: CDSL: IN-DP-CDSL-443-2008 CIN No.: U67120MH2004PLC146183 | SAMCO Commodities Limited (Formerly known as Samruddhi Tradecom India Limited) | MCX- 55190 | SEBI Reg. No.: INZ000013932 Registered Address: Samco Securities Limited, 1004 - A, 10th Floor, Naman Midtown - A Wing, Senapati Bapat Marg, Prabhadevi, Mumbai - 400 013, Maharashtra, India. For any complaints Email - grievances@samco.in Research Analysts -SEBI Reg.No.-INHO0O0005847.

Easy & quick

Easy & quick

Leave A Comment?